What’s with the Cat?

Indeed, the feline in question bears no direct relevance to Schrödinger Inc. (SDGR), the company under review.

Yet, the name Schrödinger is steeped in the legacy of a famous thought experiment that serves as a metaphor for the perplexing nature of quantum mechanics.

Devised in 1935 by Austrian physicist Erwin Schrödinger, the thought experiment sought to illustrate the paradoxes inherent in the nascent field of quantum theory.

At its heart, the experiment examines how quantum phenomena might interact with our more tangible, classical world. Schrödinger imagined a box containing a radioactive atom, a vial of poison, and, crucially, a cat. According to quantum mechanics, the atom can either decay or remain stable, but it is only when the atom decays that the poison is released, killing the cat. Until observed, the cat exists in a quantum superposition—simultaneously alive and dead—highlighting the strangeness of quantum indeterminacy.

The thought experiment became a cornerstone in the interpretation of quantum theory, challenging conventional understanding and paving the way for the many-worlds interpretation. This view posits that all possible outcomes of a quantum event occur in separate, parallel realities—each crystallizing at the moment of measurement.

That is Schrödinger’s cat in a nutshell, though I could easily lose hours debating the finer points of quantum theory, as I did during my university days.

For now, however, let’s pivot from quantum enigmas to a more grounded topic: our latest stock pick for 2025, and that is Schrödinger Inc. (SDGR).

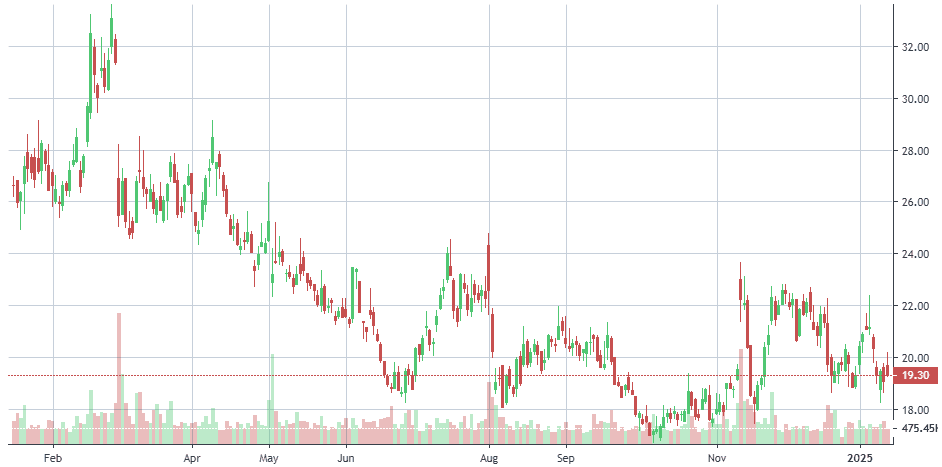

Schrödinger (SDGR) is a name we’ve followed closely since its IPO, intrigued by its potential but adhering to our usual caution with newly listed companies, especially in a market rife with volatility.

Our strategy is to wait for a few quarters before making an entry, and in this case, we believe our timing has been relatively strong, especially given the stock’s decline since its debut.

At a time when Big Pharma is grappling with revenue slumps and declining stock prices—Pfizer’s market valuation, for instance, has halved since 2021—Schrödinger stands out as a beacon of innovation. While many of its peers are fixated on cost-cutting measures, Schrödinger is unwavering in its mission to revolutionize drug discovery through the fusion of physics simulations and artificial intelligence.

Schrödinger offers a bold and disruptive vision: to target the $100–150 billion annual spend on pharmaceutical R&D. Instead of relying on the traditional, time-consuming and costly approach of synthesizing molecules in laboratories, Schrödinger harnesses advanced AI and physics models to generate billions of virtual drug candidates in silico. This methodology has the potential to streamline the process, dramatically reduce costs, and speed up the historically drawn-out timelines of drug development.

The company’s business model is two-fold: it generates recurring software revenues from its platform and anticipates royalties from drug discoveries in the coming years. While the latter will take time—management expects it to gain significant traction within six to seven years due to the lengthy FDA approval process—the former offers a more immediate path to profitability. With no imminent risk of dilution and enough reserves to fund operations for the next two to three years, Schrödinger presents an attractive risk-reward profile for investors.

The long-term appeal of Schrödinger lies not only in its innovative model but also in the company’s growing portfolio of pipeline collaborations. Though its hybrid structure—part software, part biotech—may cause some confusion among generalist investors, the company’s software revenues provide a solid foundation that offers a degree of safety. For those willing to delve into the complexities of Schrödinger’s business, the potential rewards are significant. The company has the chance to not only reshape the pharmaceutical industry but to carve out an entirely new and lucrative market.

The Trade:

It’s important to note that the healthcare sector was among the worst performers of 2024.

However, we believe the sector is primed for a strong rebound in 2025. With Schrödinger’s added AI edge, the company is poised to capitalize on this broader market recovery.

In addition to its promising software and biotech platform, Schrödinger has secured several major collaborations and partnerships, further strengthening its outlook. With the AI-driven narrative gaining momentum, we believe the company could see its share price double by year-end, approaching $40 per share.

At our core, we prefer investing in companies that tackle complex, impactful challenges, those that serve both the enterprise and consumer markets. Schrödinger is a prime example of this, having achieved product-market fit and positioning itself for exponential growth in the long term.

Schrödinger’s Business Model and Flywheel

Schrödinger Inc. operates at the intersection of software, drug discovery, and materials science, leveraging its proprietary computational platform to drive innovations across various sectors. The company’s business model is built around a unique combination of software licensing, collaborations, and a proprietary pipeline.

Software Licensing

Schrödinger’s software platform is a core component of its business, offering powerful computational tools for molecular modeling and simulation. The company licenses this software to pharmaceutical and biotechnology companies, as well as academic institutions, enabling users to accelerate their research and development processes. Schrödinger’s software is especially powerful in predicting the behavior of molecules, which aids in drug discovery and the development of novel materials. The platform helps scientists optimize molecular properties, screen large datasets for potential drug candidates, and simulate drug-receptor interactions—all critical steps in speeding up R&D efforts.

Revenue from software licensing forms a steady and recurring income stream, allowing Schrödinger to build long-term relationships with clients. These clients often renew licenses or expand their usage, driving stable growth. Licensing agreements are structured with both upfront payments and ongoing royalties, creating financial sustainability for Schrödinger.

Collaborations

In addition to licensing its software, Schrödinger actively pursues collaborations with pharmaceutical, biotechnology, and materials science companies. Through these strategic partnerships, Schrödinger is able to co-develop drug candidates and innovative materials, while its partners gain access to the company’s cutting-edge computational platform and research expertise. Notably, Schrödinger partners with leading pharmaceutical firms to apply its technology in accelerating drug discovery, with an emphasis on improving hit identification and enhancing the efficiency of preclinical development.

Collaborations are often structured to include milestone payments and royalties, as well as equity investments, particularly when Schrödinger is directly involved in drug development alongside its partners. These collaborations further fuel the company’s growth by offering both immediate financial rewards and long-term value creation opportunities through successful product development.

Proprietary Pipeline

Schrödinger’s proprietary pipeline represents the company’s most significant value driver. The firm leverages its software platform to discover and develop its own portfolio of drug candidates, focused primarily on oncology and immunology. Schrödinger uses its platform to identify novel small molecules, design drug candidates with improved properties, and advance these candidates through the preclinical and clinical development stages.

The company’s pipeline includes several promising candidates, some of which are partnered with major pharmaceutical firms for further development. Schrödinger’s proprietary pipeline creates value in two ways: first, through the potential to generate high returns if its drug candidates are successfully developed and commercialized; and second, through the strategic collaborations that often emerge from its development process, where Schrödinger partners with larger companies in licensing deals or co-development agreements.

Flywheel Effect

Schrödinger’s business model operates as a flywheel, wherein each component reinforces and accelerates the others. Software licensing generates predictable revenue, which allows the company to reinvest in its proprietary drug pipeline. Collaborations provide both financial resources and access to expertise, helping Schrödinger refine and develop its pipeline further. Successful advancements in its pipeline create additional revenue opportunities through licensing or partnership agreements, while also expanding the reach of its software platform to new industries and sectors.

This interconnected ecosystem creates a powerful feedback loop: revenue from software licenses supports R&D, which in turn strengthens the proprietary pipeline; collaborations accelerate drug discovery and development, driving more licensing opportunities, and successes in the pipeline generate further partnership interest.

As Schrödinger continues to execute on this flywheel, its capacity to grow its software business and develop proprietary drug candidates positions it for sustainable success in both the technology and life sciences sectors. This integrated approach enables the company to maintain a strong competitive position while capitalizing on the synergies between its technology, collaborations, and in-house drug discovery efforts.

Schrödinger has taken an assertive approach to growth, far from passively relying on software sales alone. Instead, it has skillfully applied its proprietary computational platform to build both a drug development pipeline and a portfolio of collaborations. A standout example is Morphic Therapeutics, which is set to be acquired by Eli Lilly in the upcoming quarter for $48 million, with Schrödinger securing not just revenue but also an ongoing royalty stream. This deal embeds Schrödinger’s innovations into Lilly’s expansive drug portfolio, solidifying its position in the biopharmaceutical ecosystem.

Rather than undertaking the costly and protracted journey through Phase 3 FDA trials, Schrödinger’s strategy is more nuanced. It aims to partner with or sell its developmental drug candidates to major pharmaceutical players. This model enables the company to generate revenue while simultaneously demonstrating the capabilities of its software platform. This dual approach diversifies Schrödinger’s income streams while ensuring that its technology becomes deeply embedded within the fabric of the biopharmaceutical industry.

As a generalist perspective confirms, Schrödinger competes at the top of its field, alongside firms like Dassault’s Accelrys. The company’s primary competitive advantage lies in its vast, computationally derived database of molecules—an asset that creates a formidable barrier to entry. Although the long-term risk of falling computational costs could erode this advantage, Schrödinger’s current head start and the limited competitive landscape solidify its strong position.

Indeed, Schrödinger’s software business alone justifies its valuation, even without factoring in its robust drug pipeline, which comprises over 25 candidates. This pipeline, however, remains a significant untapped asset. With substantial funding expected from collaborations like Morphic, Schrödinger is well-positioned to bridge any financial gaps and sustain growth. The ability to fund future drug developments through additional Phase 1 sales underscores its financial acumen, though, as always, biotech remains a sector fraught with uncertainty.

A prime example of Schrödinger’s potential lies in its 2020 partnership with Bristol Myers Squibb, which resulted in a $2.7 billion deal, including $55 million in upfront cash and additional payments tied to milestones in drug development. Schrödinger has previously struck similar deals with heavyweights such as AstraZeneca, Sanofi, and Bayer, further illustrating the strength of its drug discovery platform. This traction has led to over 10 active collaborations across the globe, some of which are in the critical stages of IND-enabling, Phase 1, or even Phase 2 clinical trials. Schrödinger has also taken equity positions in several of its collaborators and co-founded companies, such as Relay Therapeutics, creating yet another revenue stream that will likely expand over time.

Beyond drug discovery, Schrödinger’s platform also offers untapped potential in other industries, particularly in the development of new materials. Its molecular simulation capabilities are applicable to energy sectors like battery development, fuel cells, hydrogen storage, and organic electronics, as well as aerospace and semiconductors. If Schrödinger were to forge partnerships with disruptive companies in industries like electric vehicles or alternative energy, the potential for new revenue streams is immense.

With $380 million in cash and zero debt, Schrödinger enjoys the financial flexibility to pursue research and development opportunities in new sectors. This financial sustainability, combined with its first-mover advantage, positions Schrödinger to continue expanding its footprint across multiple industries.

What truly sets Schrödinger apart is its synergistic business model and clear vision. The company remains focused on refining its software platform, which, in turn, drives better outcomes for its commercial customers. This creates a virtuous cycle: improved results attract new customers, who fund Schrödinger’s internal drug discovery pipeline. This strategy of continuous improvement and reinvestment positions Schrödinger for long-term, exponential growth.

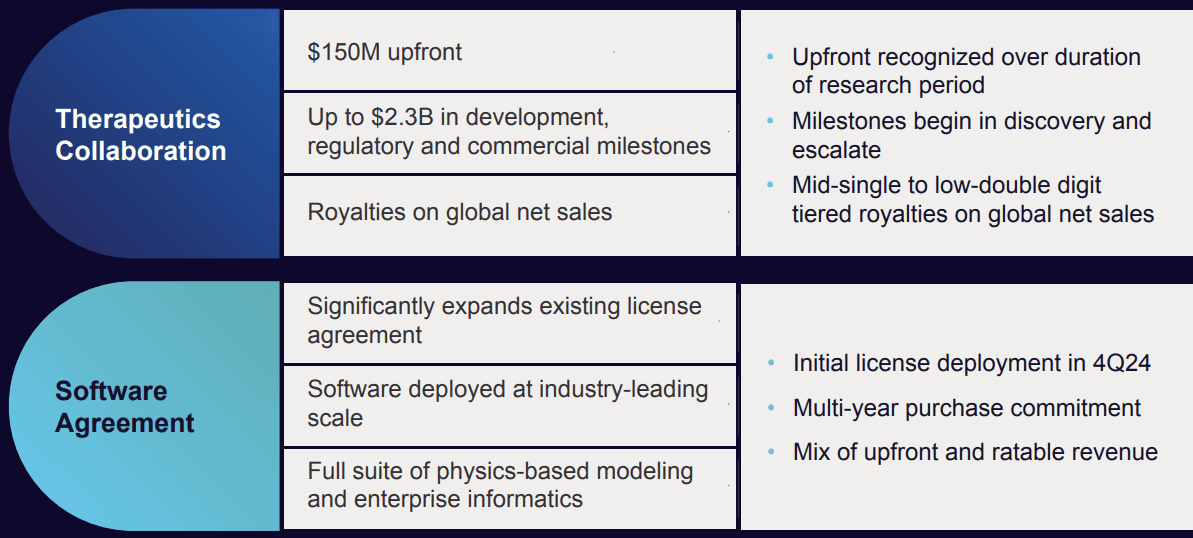

In a notable endorsement of Schrödinger’s capabilities, Novartis has pledged $150 million upfront to collaborate on a portfolio of discovery-stage programs, leveraging Schrödinger’s advanced computational chemistry platform. This multi-year partnership will combine their expertise to identify and advance drug candidates for Novartis’s core therapeutic areas. Schrödinger will focus on early-stage discovery, while Novartis will take charge of clinical development, manufacturing, and global commercialization.

The stakes are high. Schrödinger stands to earn up to $892 million in research and regulatory milestones and a further $1.38 billion in commercial payouts, alongside tiered royalties reaching into low double digits on net sales. Although details remain undisclosed, this partnership reflects Big Pharma’s growing reliance on computational R&D, which promises efficiencies that traditional methods cannot match.

Schrödinger’s pipeline, currently dominated by oncology, also extends into immunology and neurology. Targets like NLRP3 and LRRK2 have already captured the attention of industry heavyweights, including Biogen and Bristol Myers Squibb, underscoring the relevance of Schrödinger’s assets.

In essence, Novartis’s investment symbolizes confidence in Schrödinger’s physics-based approach to drug discovery, positioning it as a key player in reshaping pharmaceutical R&D. This collaboration could redefine the boundaries of computational biology, with billions riding on its success.

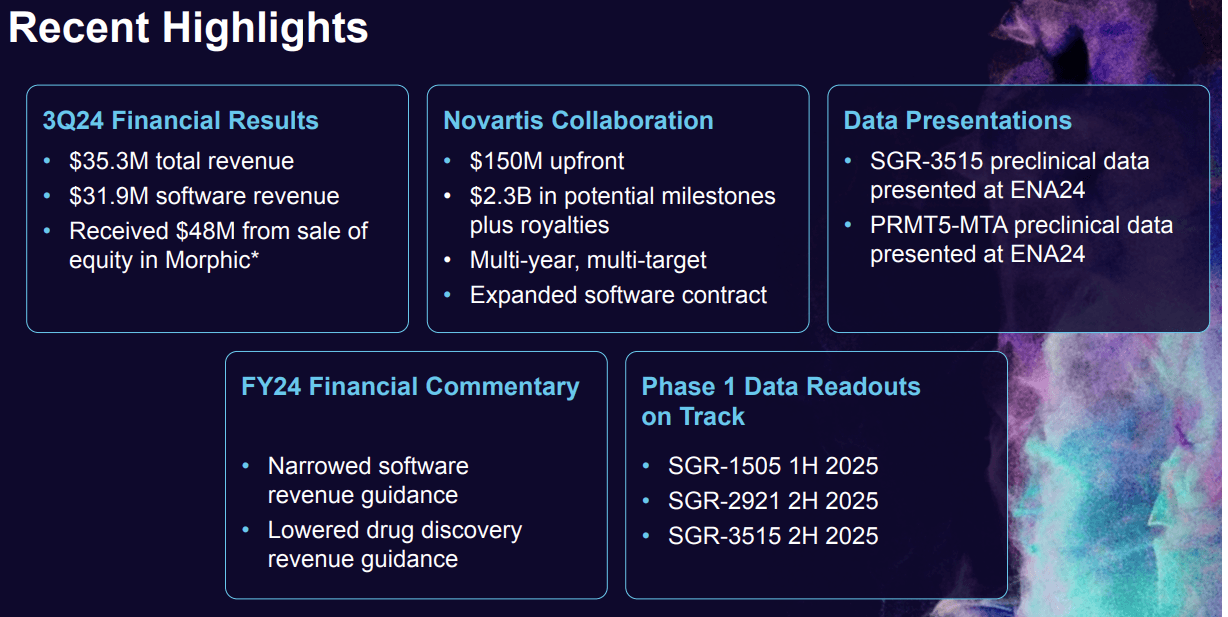

Schrödinger’s Q3 2024 results illustrate a company caught between growth prospects and operational challenges. Total revenue for the quarter reached $35.3 million, down from $42.6 million in the same period last year. The dip was largely driven by a sharp decline in drug discovery revenue, which fell to $3.4 million from $13.7 million in 2023. This was primarily due to revenue recognition from collaborations that have since wound down.

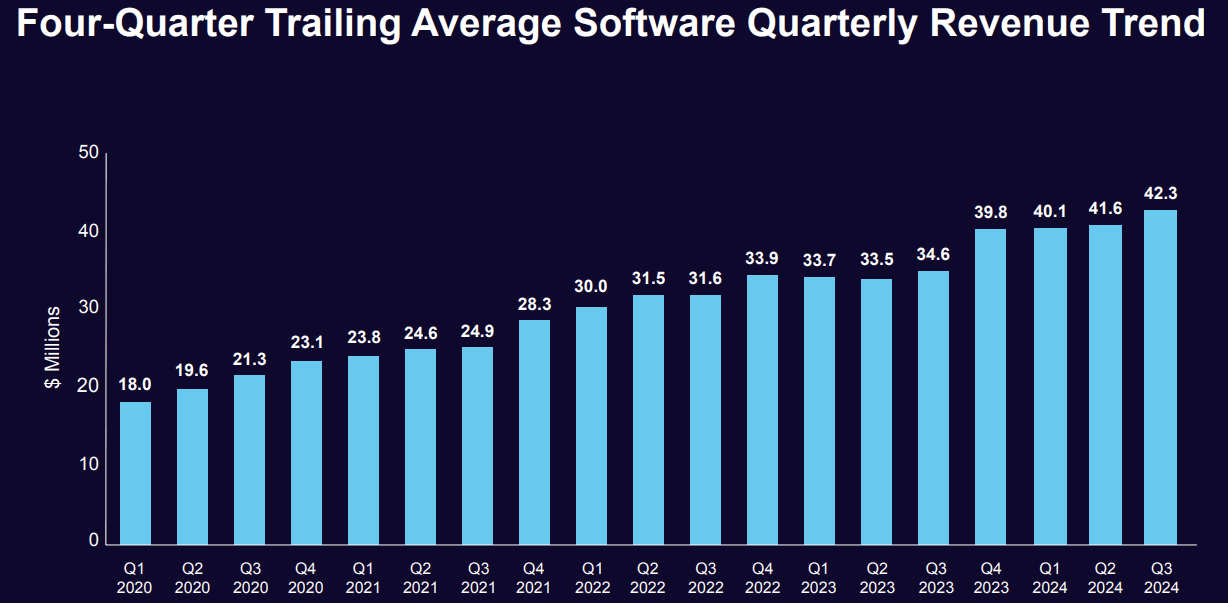

On a more positive note, software revenue continued its upward trajectory, increasing 10% year-over-year to $31.9 million. This growth was fueled by strong demand for hosted licenses, though it was somewhat tempered by a reduced proportion of longer-term, on-premise contracts. However, despite this positive revenue shift, software gross margins contracted to 73%, a reflection of the profitability pressures tied to Schrödinger’s predictive toxicology initiatives.

Operating expenses saw a rise, climbing to $86.2 million from $79.8 million in the same quarter of 2023. This was driven largely by increased investment in research and development. The silver lining came in the form of other income, which surged to $30.2 million, a dramatic improvement from last year’s $8.7 million expense. This boost, largely driven by favorable returns on equity investments, helped mitigate the net loss, narrowing it to $38.1 million compared to $62 million a year ago.

With a cash position of $398.4 million in marketable securities as of September 30, Schrödinger remains well-funded, allowing it to continue its groundbreaking work in computational drug discovery. The company’s physics-driven platform is accelerating drug development timelines—transforming what traditionally takes years into mere months—while optimizing molecule properties for clinical trials.

This blend of innovation and fiscal prudence underscores Schrödinger’s potential as a transformative force in the pharmaceutical sector, although margin pressures and cost management remain areas to watch.

A company’s ability to maintain growth, fend off competitors, and secure long-term viability is often determined by its financial model. Schrödinger has crafted a model that not only facilitates customer retention but also drives down the cost of acquiring new customers through net revenue expansion. At the core of this strategy is its physics-based computational platform, which helps collaborators discover high-quality molecules faster, more accurately, and at lower costs compared to traditional methods. What may take competitors five or six years to bring a drug to clinical trials, Schrödinger can often accomplish in just two or three years, with an optimized property profile for the trial.

In addition to its patents that safeguard its innovative platform, Schrödinger’s software-as-a-service (SaaS) model lowers customer acquisition costs. As existing customers expand their use of the platform over time, Schrödinger benefits from recurring revenue streams. Moreover, the company continues to gain additional revenue through its internal drug discovery programs and collaborative partnerships, further enhancing its financial stability and market positioning.

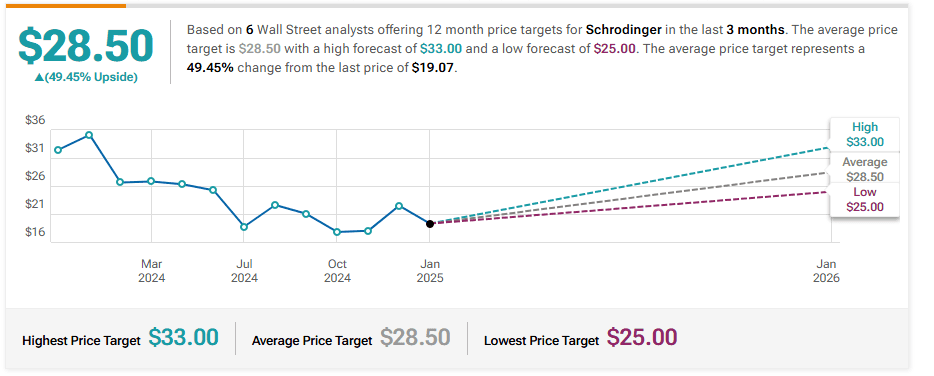

BMO Capital Maintains Outperform on Schrodinger, Raises Price Target to $28

Morgan Stanley Maintains Equal-Weight on Schrodinger, Lowers Price Target to $30

Keybanc Maintains Overweight on Schrodinger, Lowers Price Target to $25

Leerink Partners Initiates Coverage On Schrodinger with Outperform Rating, Announces Price Target of $29

Citigroup Maintains Buy on Schrodinger, Lowers Price Target to $37

Craig-Hallum Maintains Buy on Schrodinger, Lowers Price Target to $30