2025 is here, and early indicators suggest the year will be nothing short of tumultuous. A new U.S. president takes office on January 20, pledging to raise tariffs on nearly all of its trading partners, including Canada—a prospect that promises to create significant market turbulence.

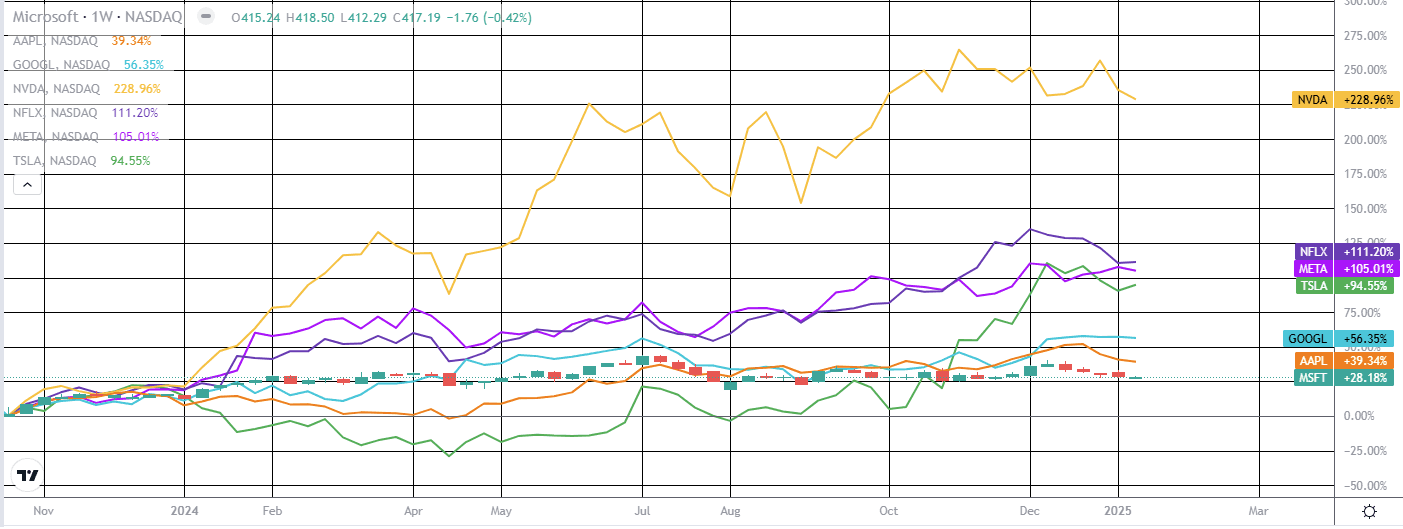

Compounding the uncertainty is the fact that we enter the year with a market that is historically expensive, particularly among the U.S. “Magnificent Seven” stocks, which are trading at roughly 60 times trailing earnings.

A key determinant of the equity landscape in 2025 will be whether President Donald Trump follows through on his threat to impose tariffs on certain trading partners, including Canada. Such a move could spark significant volatility, but the impact is unlikely to be felt uniformly across sectors. The most vulnerable, in our view, are those that have experienced the most substantial gains in the previous cycle, notably big tech stocks. By contrast, less scrutinized sectors appear to offer more promising prospects.

While mega-cap AI stocks have been the driving force behind market returns in recent years, leadership is shifting toward companies that are using AI to create tangible efficiencies. The new administration’s focus on deregulation and tariff-driven policies may provide a boost to smaller, domestically focused firms, which are less vulnerable to international trade disruptions compared to their larger counterparts with heavy foreign revenue exposure, such as Apple.

This shift should reduce market concentration and open doors to alpha-generating opportunities. Active traders will likely play an important role in identifying undercovered companies that are adopting AI to drive productivity and secure competitive advantages. As the adoption of AI accelerates, fueled by declining costs, companies leveraging these technologies stand to benefit from enhanced productivity and improved market positioning.

In addition, with interest rates stabilizing and valuations becoming more attractive, real assets like real estate and infrastructure are poised to offer compelling opportunities for growth, income stability, and protection against inflation—particularly in a climate of policy uncertainty.

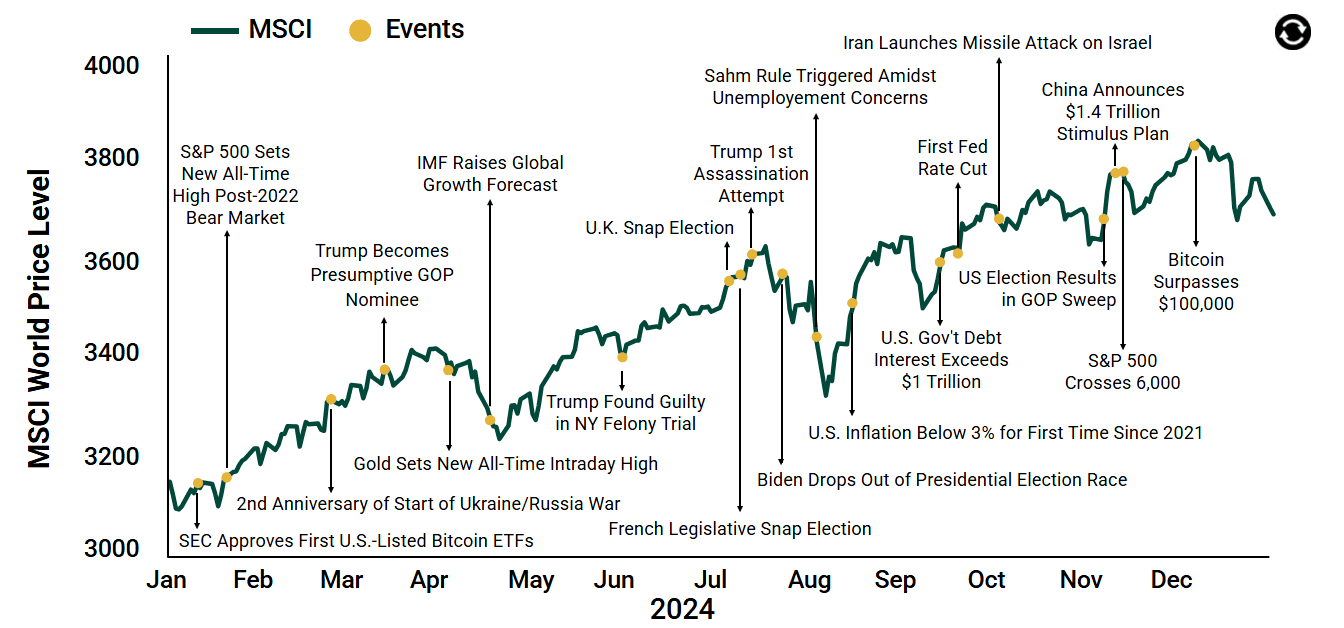

Looking back on 2024

When it comes to media headlines, there is rarely a quiet moment. 2024 proved no exception.

A steady stream of sensational stories sparked fear—and, at times, greed—among investors. Yet, despite the relentless barrage of narratives and the occasional setback, the markets continued their upward march.

A small sampling of the year’s headline moments is captured in Exhibit 1. These are but a fraction of the news cycles that stocks absorbed and moved beyond. For short-term focused investors, many of these events could have served as a catalyst to abandon long-term goals and exit the market—an all-too-common misstep. However, those who maintained discipline in the face of an excess of news were ultimately rewarded.

While we recognize that there are legitimate reasons to adjust one’s investment strategy, overreacting to headlines designed to provoke emotion is not one of them.

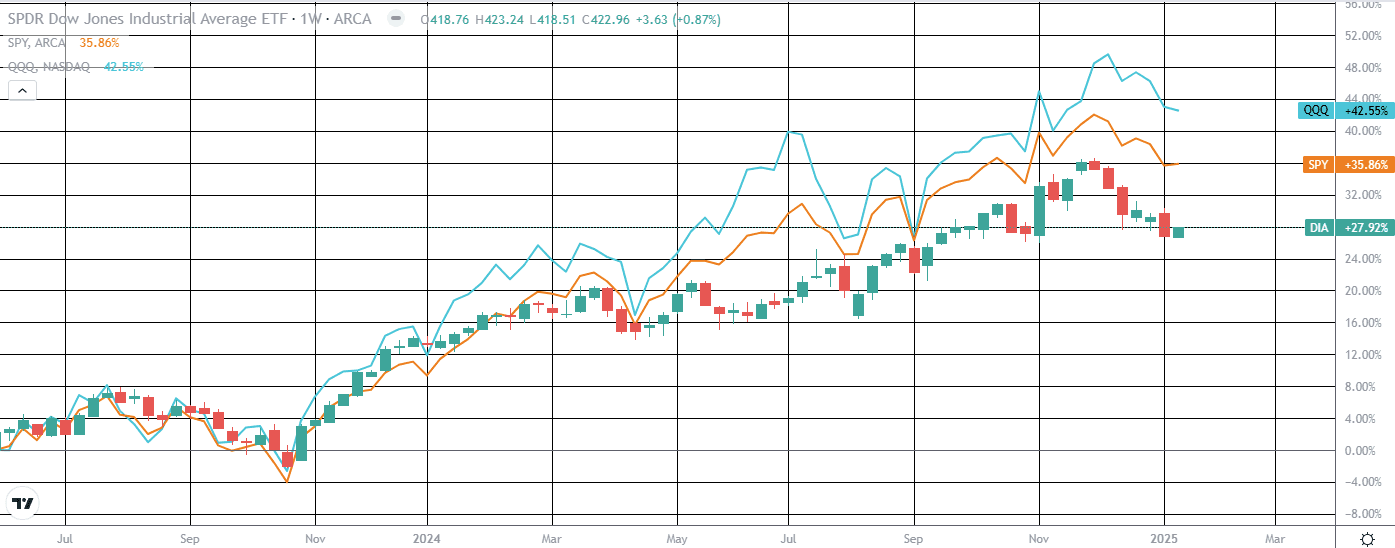

For investors, 2024 proved to be a year of surprises, upending many of the predictions made by economists and strategists at the outset. A standout example was the remarkable performance of the S&P 500 Index, which was set to close the year up more than 25%, far surpassing Wall Street’s expectations and marking one of its most robust annual performances in the past quarter-century.

The year had much to offer investors. Inflation and interest rates declined, corporate earnings remained strong, and the three major stock indexes set new records. Despite occasional volatility, the stock market was poised for its second consecutive year of double-digit returns.

Despite a few hiccups and minor deviations from the expectations set in late 2023, 2024 was a solid year. The economy grew above trend in both Q2 and Q3, with optimistic projections for Q4. Investors also welcomed the Fed’s decision to lower interest rates in September, while sentiment across both equity and fixed-income markets largely remained “risk-on.” The S&P 500 continued to hit all-time highs, and corporate credit spreads remained tight.

In short, 2024 was a year that challenged conventional economic models and assumptions. Given the unpredictability of the environment, prudent long-term investors should remain focused on portfolio risk management as they head into 2025.

Regime change arrived, though not quite as we expected. Earlier in 2024, we had fixated on the “Magnificent Seven.” Could they continue to bear the weight of the market? At times, it seemed as though a shift was imminent—especially in July, when small-cap stocks appeared poised for a resurgence, or after the market reacted tepidly to a solid, if not stellar, Nvidia earnings report. These, however, proved to be little more than distractions. Big Tech continued its march forward.

The real regime change, however, manifested through what we might call the “Trump trade.” As prediction markets began to price in his potential victory, a broad-based bull run emerged, with small-caps, Bitcoin, Tesla, and bank stocks enjoying notable gains. While this momentum has since cooled somewhat, investors are still factoring in earnings support from tax cuts, deregulation, and a flourishing economy. Only industries grappling with distinct challenges, such as energy, materials, and healthcare, have been notable laggards.

The question of whether AI represents a bubble has occupied our minds. If it is, the timing of its eventual deflation remains elusive. Markets, however, have shown increasing nervousness with each earnings report, particularly as capital expenditure on data centers and AI infrastructure ramps up. We foresee this trend continuing into the next year, with the possibility of significant downsides—perhaps even a sharp correction.

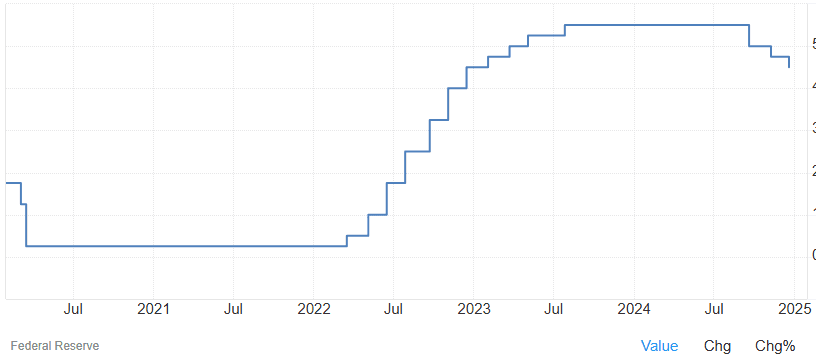

U.S. exceptionalism remained a theme as the year drew to a close, bolstered by low layoffs and improving corporate earnings that suggest a soft landing. The recent election results, however, introduce uncertainties around tariffs, immigration, and pro-market policies like tax cuts and deregulation. Nonetheless, we anticipate a measured approach. A post-election rebound in business confidence provides some optimism. As for the Federal Reserve, we expect a gradual reduction in interest rates toward a new “normal” of 3.25%, with market pricing reflecting these expectations.

And now, a word on the Fed as we reflect on 2024…

After enduring the most rapid tightening of monetary policy by the Federal Reserve in nearly four decades, markets embraced the news of disinflation. Throughout much of 2024, inflation appeared to be heading in the right direction, but it stalled mid-year, overshooting the expectations set earlier in the year.

Unlike previous cycles, where the Fed’s monetary policy moves were deliberate and designed to preemptively address future inflation risks, this tightening cycle took on a much more rapid and unorthodox character. The speed and scope of these adjustments were far from typical.

Despite this, growth, particularly in the U.S., remained surprisingly resilient throughout 2024. We expect this momentum to carry into 2025. The labor market has maintained a healthy balance, and should the equity rally persist, coupled with growing investments in emerging technologies, we foresee increased confidence among both firms and households to invest and spend. This, in turn, should slow, but not completely halt, the disinflationary process.

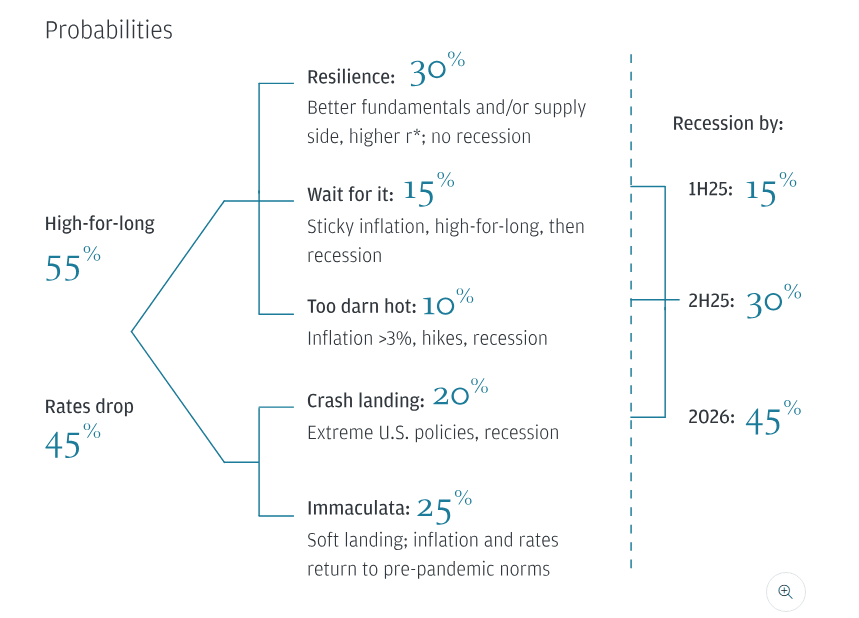

Moreover, we anticipate that the current rate easing cycle will differ from its predecessors—more gradual and protracted, shaped by three key themes.

Potential Fed Pause We foresee potential price pressures emerging from business and household spending, alongside an uptick in tariffs on U.S. imports and fiscal stimulus, which could raise concerns about inflationary pressures.

However, with wage growth continuing to soften and tariffs likely to be a temporary, one-off shock rather than a sustained inflationary force, we expect the Fed to pause by mid-2025 rather than pivot to another tightening cycle.

Heading into 2024, the question of whether the Fed—or other major central banks—would cut short-term interest rates was a hot topic among investors. Some argued that rate cuts were necessary for the bull market to continue. But what impact, if any, do rate cuts—or hikes—have on stocks looking ahead?

In our view, neither rate cuts nor hikes serve as reliable indicators of future stock market returns. Historical evidence suggests that turning points in Fed policy—when rate hikes or cuts begin—haven’t been decisive in shaping stock performance.

To gauge the effect of a rate change, one need only look at the 12-month period following the first rate hike (green dots) or rate cut (gold dots) of a cycle. Since 1950, forward returns have been positive just over 70% of the time.

In contrast to popular belief, stocks have tended to perform better following rate hikes than after rate cuts. That said, returns have still often been positive after the initiation of a cutting cycle, underscoring the fact that it’s usually a favorable environment for investors—as we witnessed in 2024.

Top Factors Likely to Influence Stocks in 2025

As we look toward the year ahead, two central themes emerge as likely drivers of financial markets: the economic policies of the incoming Trump administration and the ongoing evolution of innovative technologies.

1. U.S. Growth and Policy Trade-offs

The U.S. economy is projected to grow at a trend-like pace of around 2.0% in 2025, reflecting the delayed impact of the Federal Reserve’s aggressive tightening. Core personal consumption expenditures (PCE) inflation is expected to move closer to the Fed’s 2% target, while the central bank gradually eases rates, with the fed funds rate likely reaching 3.25% by year-end—an alignment with its neutral level.

The policies of the new Trump administration present a delicate balancing act. On the one hand, tax reforms and deregulation are expected to stimulate growth, particularly in domestic and cyclical sectors. On the other, tariffs and immigration restrictions could potentially provoke a stagflationary shock, forcing the Fed to reconsider its stance and contemplate a rate hike if economic conditions weaken.

Our working assumption is that the administration will likely refrain from aggressively pursuing policies that could exacerbate inflation risks. One clear takeaway from the election is that U.S. voters were displeased with the inflationary pressures under the Biden administration. While tariffs and immigration restrictions are expected, their scope will likely be limited by the inflation outlook. Overall, we anticipate that the policy mix will prove supportive of business confidence, potentially driving a rebound in capital markets and providing favorable tailwinds for private assets.

2. Market Sentiment and Valuations

The market outlook for 2025 will be shaped by three primary factors: the elevated level of the S&P 500’s forward P/E (price-to-earnings) ratio, the potential for further U.S. dollar strength, and the trajectory of U.S. Treasury yields.

Equity valuations in the U.S. are currently elevated, making the market susceptible to negative surprises. Furthermore, any continued strength in the U.S. dollar could present challenges for emerging markets. Prolonged U.S. Treasury yields above 4.5% could exert pressure on equities, diminishing the earnings yield advantage that stocks have enjoyed over bonds since 2002.

The road ahead for investors will require navigating these complex factors, as the balance between policy, growth, and valuations will likely define the course of markets in 2025.

Correction to Start the Year

We believe equity markets are poised for a potential correction at the outset of 2025. Although the S&P 500 is down only 5% from its record high set on December 6, there are mounting concerns that volatility will surge this year. A new U.S. President in the White House, coupled with historical data suggesting the current rally is becoming long in the tooth, creates an environment ripe for recalibration.

Moreover, when you factor in the strong stock performance of the past year and the tail end of tax-loss harvesting season, a pullback seems only logical.

Other indicators also point to the possibility of a near-term market setback. Six of the eleven stock market sectors are currently trading above their 200-day moving averages, down from all eleven in late December. Additionally, another measure of market breadth—the percentage of S&P 500 stocks above their 200-day moving averages—has sharply declined over the past month, from approximately 76% to 55%.

The next crucial test for the markets begins as companies report their earnings. While we remain unconcerned about fourth-quarter results, as economic growth appears to have remained resilient, we do have reservations that management teams may seek to lower expectations for 2025 earnings growth. The rate of economic expansion is set to decelerate, and this may prompt a more cautious outlook.

However, we see this as a potential opportunity to buy select stocks at discounted levels before the market inevitably embarks on its next leg upward.