As the year began with what seemed a conventional Presidential election landscape, the summer months have brought a series of political upsets. Former President Donald Trump sailed smoothly to secure his third Republican nomination. Just after the July Republican National Convention—where Trump chose Ohio Senator JD Vance as his running mate—the political winds shifted. Democratic President Joe Biden announced his withdrawal from the race, endorsing Vice President Kamala Harris to succeed him. In short order, Harris secured the Democratic nomination and selected Minnesota Governor Tim Walz as her Vice Presidential candidate.

The newly minted Democratic ticket has injected fresh uncertainty into what was once a predictable contest. While Trump emerged from the GOP convention with significant momentum and a lead in key battleground states, Harris’ campaign swiftly gained traction. Polling now suggests the race is once again a close contest.

As the Presidential race intensifies, the broader implications for down-ballot races remain unclear. Control of Congress hangs in the balance. One-third of the Senate seats—under narrow Democratic control—and all 435 seats in the House of Representatives—where Republicans hold a slim majority—are also up for grabs. The margins are razor-thin, and the outcome could lead to either unified control of both chambers and the presidency by one party or a continuation of today’s divided government.

This election cycle, with its political twists, poses questions for investors. In a polarized climate, the uncertainty can stir concerns about market performance. Yet, history has shown that politics, while a source of volatility, is not a reliable long-term determinant of market direction. Over the past several election cycles, the markets have demonstrated resilience, with neither party’s control dictating sustained outcomes.

In fact, the market often favors gridlock—a scenario in which legislative action stalls, reducing the likelihood of sweeping regulatory changes. Investors seeking certainty in uncertain times may find comfort in the predictability of gridlock, which tempers market fears of sudden regulatory shifts.

While the 2024 election outcome remains uncertain, and Congress hangs in the balance, investors would do well to focus on enduring fundamentals: economic growth, inflation, and corporate earnings, rather than the political noise. For markets, it’s often less about who governs and more about how policy shifts—or stalls.

The stock market’s performance is influenced by a labyrinth of factors, many of which have little to do with the occupant of the White House or the composition of Congress. Yet, historical data suggests a curious tendency: as a president edges closer to re-election, stock prices often ascend, as if markets anticipate the stability that continuity promises.

While the headlines may seize upon election dramas, it is the underlying fundamentals—such as inflation, the broader economy, and the Federal Reserve’s hand—that dictate the market’s true course. These forces wield far more influence on long-term performance than the transient effects of electoral cycles, a truth that investors are reminded of every four years.

However, the short-term ripples of elections cannot be entirely dismissed. Multiple studies have noted that national elections can and do provoke short-term market reactions. The U.S. economy, a $28 trillion behemoth fueled by consumer spending, is not re-engineered overnight by a new administration. Instead, shocks come from external pressures—interest rate fluctuations, financial imbalances, and unforeseen global events—which may deliver unwelcome surprises to investors.

The annals of market history offer a telling narrative: in the past 40 years, only once—following the dot-com bubble burst in 2000—have markets delivered negative returns 12 months after an election. For instance, after the 2008 election, despite a steep decline three months in, markets clawed back to a positive return within the year. In both cases, it was external economic turbulence, rather than electoral politics, that drove the market downturns.

Donald Trump’s presidency provides a notable deviation from the expected first-year slump in stocks. His administration’s push for tax cuts in 2017 ignited a rally that saw the S&P 500 leap 19.4%. Yet, his second year in office saw a reversal, with a 6.2% decline, only for the third year to deliver a stellar 28.9% surge. Here, too, the narrative transcends politics, highlighting the market’s fickle relationship with electoral cycles.

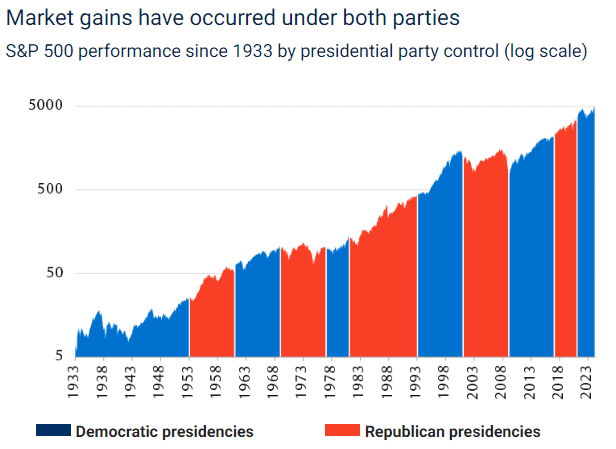

The U.S. stock market has long been an indifferent spectator to the ebb and flow of political tides, rising under both Republican and Democratic administrations, whether marked by controversy or relative calm. As the accompanying chart illustrates, equities have climbed through a variety of presidencies, sometimes despite the prevailing political winds.

There have, of course, been periods of struggle. The 1970s, for instance, witnessed anemic market performance during the administrations of Richard Nixon and Gerald Ford (both represented in red), and later under Jimmy Carter (in blue). Yet, the broader trend from 1933 onward reveals a market that has shown resilience, climbing significantly during both Republican and Democratic tenures.

Since 1953, the S&P 500 has tended to perform best under a Democratic presidency coupled with a divided Congress or one under Republican control. Curiously, the market has also fared well during periods of Republican dominance. The lesson, perhaps, is that markets are less concerned with who governs than with how capital flows, interest rates move, and economic fundamentals unfold.

As previously noted, analyzing market returns under various political regimes offers scant insight into the underlying reasons for economic performance or future market direction. Political configurations, while tantalizing to track, are often poor guides to future investment outcomes.

The charts below paint a broad picture of real GDP growth and S&P 500 returns under Republican (red), Democratic (blue), and divided governments, where no single party controls the White House and both chambers of Congress. Since 1947, real GDP has averaged 2.8% under Republican administrations and 4.0% under Democratic ones. Meanwhile, the S&P 500 has returned 12.9% under Republican rule and 9.3% during Democratic tenures.

At first glance, one might conclude that the economy thrives better under Democrats while markets fare better under Republicans. However, such a simplistic reading ignores the context: Republicans have controlled the full government just 11% of the time since World War II, spanning disparate macro environments from the 1950s to the early 2000s and just before the pandemic. In contrast, Democrats have held power 29% of the time, largely in the post-WWII era and the 1960s, with only six years of control in the last three decades.

More instructive, perhaps, is the prevalence of divided government—the most common configuration—under which the economy has grown at an annualized rate of 2.7%, while the S&P 500 has delivered a respectable 8.3% annualized return. This suggests that markets and economies are less beholden to party politics than to the broader forces of capital, productivity, and innovation that transcend Washington’s partisan divide.

Conventional wisdom might suggest that a sweeping victory by either party would send markets into a tailspin. Yet, the data firmly contradicts this notion. No statistically significant link was found between single-party control and disruptive market performance. In other words, markets, indifferent to political consolidation, appeared untroubled by electoral sweeps.

What did emerge were three divided-government scenarios that held statistical significance:

A Democratic president and a fully Republican-controlled Congress.

A Democratic president with split-party control of Congress.

Both outcomes coincided with positive absolute returns, surpassing long-term averages. In contrast, a Republican presidency coupled with full Democratic control of Congress corresponded to positive returns, albeit modestly below long-term trends.

For all the fixation on electoral outcomes, the analysis underscores that more potent forces—such as inflation trends, economic fundamentals, and Federal Reserve policy—consistently exert a greater influence on the market than partisan configurations in Washington.

The stock market, it seems, has its eye on bigger variables than who’s occupying 1600 Pennsylvania Avenue.

As The election approaches, there are a host of issues likely to command the market’s attention, with a particular focus on economic and foreign policy, as well as sector-specific developments.

Wall Street’s preoccupations often differ from those of the electorate at large, as the market is less concerned with social issues such as crime, border security, and abortion than with factors that directly influence corporate profits and growth, particularly for the S&P 500.

While the economy and the broader equity market are more difficult to sway with the results of an election, certain sectors health care, traditional and clean energy, aerospace, and defense—are notably sensitive to the outcomes, depending on the candidate’s policy platform.

Key Market Concerns:

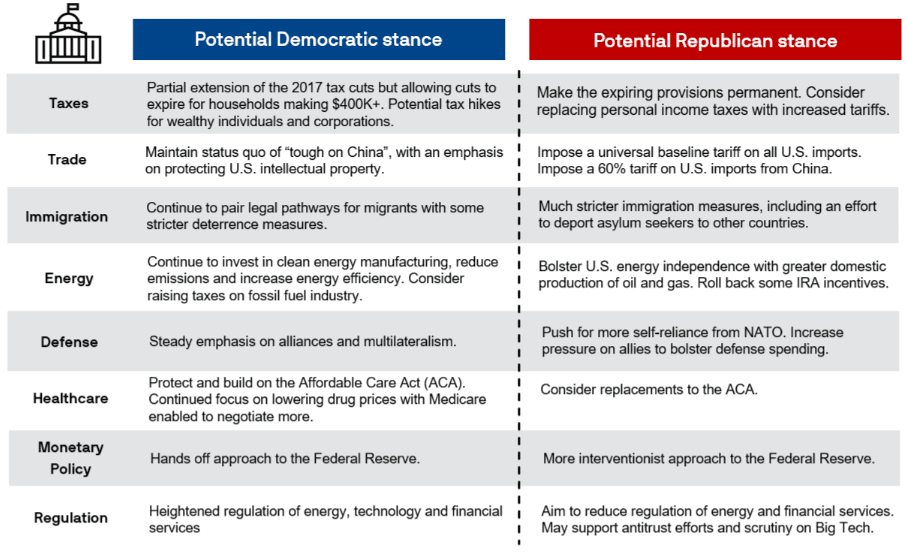

In the grand scheme, policy shapes the market more profoundly than politics itself. Below is a snapshot of how Democratic and Republican approaches may diverge across key economic issues:

Taxes

Absent the pressures of a recession or pandemic, it’s unlikely that the next administration will push for sweeping fiscal reforms. However, the expiring provisions of the 2017 Tax Cuts and Jobs Act (set for 2025) offer the next president an opportunity to revisit tax policy. Donald Trump favors making these tax cuts permanent and may propose further tariffs as offsets. Kamala Harris has signaled interest in allowing tax cuts for high earners to expire, expanding the child tax credit, and revising estate tax rules—potentially with further increases in taxes on the wealthy and corporations.

Geopolitics

On foreign policy, China remains the target of bipartisan ire, though the two parties diverge on approach. Trump, for instance, may extend leeway to Israel amid its conflict with Hamas, while pursuing a more confrontational stance on trade with Europe and Japan. Harris, on the other hand, may offer greater diplomatic flexibility with Europe while maintaining a firm posture toward China.

Immigration

Trump’s restrictive immigration policies could tighten labor markets and stoke inflationary pressures. A labor shortage might temper economic growth, though this impact would likely be moderate. Immigration remains a flashpoint in determining the size and pace of new entrants into the workforce.

Trade

Trade policy, particularly with China, stands as one of the few areas of bipartisan agreement. Democrats would likely maintain the tough rhetoric on China, while considering additional tariffs on Chinese steel and aluminum. Trump, however, might take an even more aggressive line, proposing broader tariffs on all U.S. imports and imposing severe levies on Chinese goods, thus influencing global trade flows.

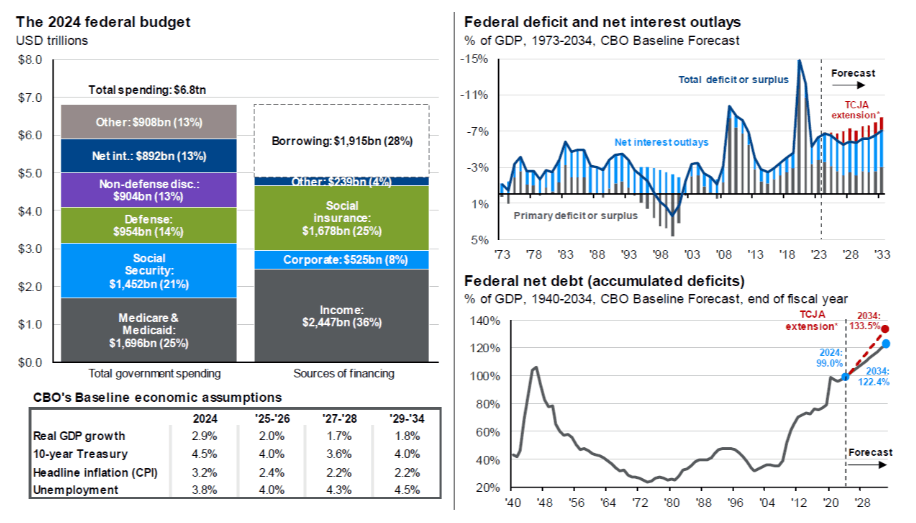

Deficit Spending

By mid-2025, the debt ceiling will once again need to be raised, setting the stage for renewed debate over U.S. debt and deficits. Market observers speculate that Trump’s approach to fiscal matters displays a certain nonchalance toward deficit expansion, which could exert upward pressure on interest rates, in contrast to a more restrained posture from Kamala Harris. Trump’s emphasis on repatriating manufacturing to American soil, paired with a willingness to tolerate larger deficits, hints at a future marked by higher interest rates, potential Federal Reserve interventions, and a gradual uptick in inflationary pressures.

Regulatory Policy

Trump’s signature deregulatory stance has always favored sectors like financial services and energy, particularly with liquid natural gas (LNG) exports expected to thrive under his administration. The light regulatory touch that characterized his presidency would also serve to support emerging industries, such as artificial intelligence, though incrementally. Drug pricing reforms, a rare point of bipartisan consensus, are likely to see little variation between the candidates’ platforms in 2024.

Regardless of who claims the presidency, the geopolitical landscape will likely remain tense, especially between the U.S. and China. Both nations will continue leaning on industrial policy to safeguard domestic interests, with further restrictions on Chinese-owned companies potentially exporting from third-party countries, such as Mexico or East Asia. Additional investments stemming from the CHIPS Act are anticipated in 2025, as nations scramble to bolster semiconductor manufacturing capacity.

Market Implications

Election years often provoke speculation about portfolio adjustments—investors toggling between defensive strategies for anticipated volatility or seeking opportunities in sectors that may benefit from specific policy shifts. But reliably constructing sector-specific strategies based on political outcomes remains elusive.

The 2020 election provides a telling case. Biden campaigned on aggressive climate policies and renewable energy expansion, culminating in the passage of the historic $369 billion Inflation Reduction Act. Meanwhile, Trump’s tenure emphasized traditional energy. Yet, sector performance defied expectations: under Trump, the S&P 500 Energy index fell by 40%, while the S&P 500 Global Clean Energy index soared by 275%. Under Biden, the inverse occurred—S&P 500 Energy nearly doubled, while clean energy slumped by 50%.In the end, it was macroeconomic forces, not political intentions, that dictated market performance. Shifts in supply-demand dynamics and interest rates outweighed the White House’s policies in determining sectoral outcomes.

Monetary Policy Matters More

For all the attention lavished on the presidency, it’s the monetary policy of the Federal Reserve that plays the greater role in shaping the economic landscape. The old market maxim still rings true: “Don’t fight the Fed.” Historically, presidents have been beneficiaries or casualties of monetary conditions far more than their own policy initiatives. President Reagan and President Clinton rode the tailwinds of falling interest rates to economic success. Conversely, both President George H.W. Bush and President George W. Bush were hampered by the Federal Reserve’s tightening, inverted yield curves, and eventual recessions. President Obama enjoyed a favorable interest rate environment for most of his tenure, except for a brief period in 2015-2016. President Trump, on the other hand, encountered a tightening Fed in his first two years, adding a layer of complexity to his administration’s early economic policy.

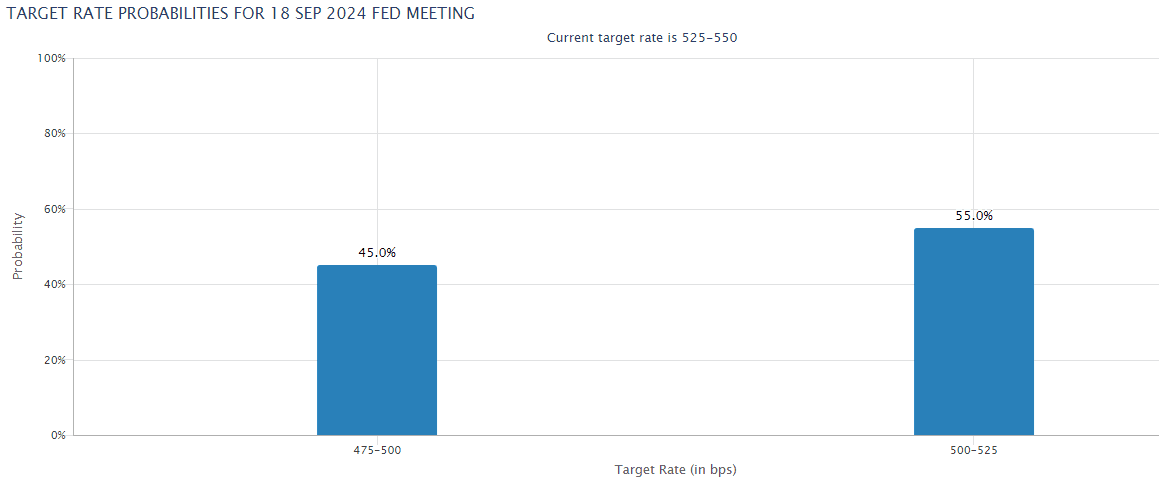

When the Federal Reserve convenes for its final pre-election meeting on September 17, the outcome could sway the direction of the 2024 race and set the trajectory for the American economy. Financial markets widely anticipate the first rate cut since the dramatic lowering in March 2020 during the COVID-19 crisis. However, whether this will be a modest 25 basis point reduction or a more assertive 50-point cut remains undecided. A crucial jobs report, expected this Friday, will play a pivotal role in guiding the Fed’s course.

Both the Harris and Trump campaigns are undoubtedly marking that report day on their calendars. A stronger-than-expected jobs report would bolster Vice President Kamala Harris’s case that the economy is on track, the Fed is poised to ease rates, and the Biden-Harris administration is fostering a robust job market with stable inflation. Conversely, a weak report would offer former President Trump a political lifeline, allowing him to criticize the economy’s fragility and portray the Fed as ineffective. Trump has voiced his preference for a bygone era when the president exerted more direct control over the Fed’s decisions, signaling his desire to reshape the institution’s role in the future.

The Fed’s Influence Over Political Developments

In assessing the interplay between political developments in Washington and the broader $28 trillion U.S. economy, we find that the actions of the White House and Capitol Hill are not typically the prime drivers of economic performance or the fortunes of most S&P 500 companies.

Instead, it is the Federal Reserve’s monetary policies that wield a more decisive impact. Historically, the Fed’s actions shape the economy, inflation, bank lending, and credit availability far more significantly than any legislative or executive measures. The Fed’s decisions set the stage for the business cycle, which in turn exerts a substantial influence on corporate profit growth—the fundamental driver of stock market performance.

Moreover, the Fed’s policies are pivotal in determining U.S. bond market performance and increasingly affect the policies and outcomes of other central banks in developed markets, influencing global bond markets as well.

The cyclical nature of U.S. economic activity—from the initiation of growth phases to the peaks and troughs of recessions—has also historically been a major determinant of financial market returns.

In essence, while political dynamics can have their moments of impact, U.S. financial markets are predominantly shaped by short-term Fed policies and, over the longer horizon, by broader economic trends, technological innovation, and corporate profitability.