Capital markets have been awaiting clarity on two critical bottlenecks to mergers and acquisitions (M&A): monetary policy and regulation. As these factors begin to normalize, the potential for a surge in dealmaking grows, fueled by a generational technology revolution, a need for liquidity, and corporates eager to reshape their portfolios through M&A. However, volatility is expected as markets grapple with uncertainties around tariffs, geopolitics, and other external risks.

Private equity firms are sitting on a staggering $2 trillion in uncalled capital, accumulated since the 2021 peak in global M&A activity, which reached $5.9 trillion. Following a sharp drop in 2022, the market has remained quiet, but signs of activity are returning. The high interest rates of recent years have stifled deal-making, leading to a slowdown in exits for private equity in 2023 and 2024.

However, take-private transactions continue to drive sponsor M&A activity, with a 21% year-on-year increase, accounting for 30% of total buy-side volumes in 2024. Globally, take-privates have been particularly strong in Europe, particularly the UK, where deal volume surged 84% in 2024, driven by technology sector activity.

Despite a still-attractive valuation environment, the true acceleration in deal activity is expected to occur after the first quarter of 2025, when market conditions and interest rates stabilize. The momentum in take-privates and capital deployment should pick up once the market adjusts to the changing dynamics.

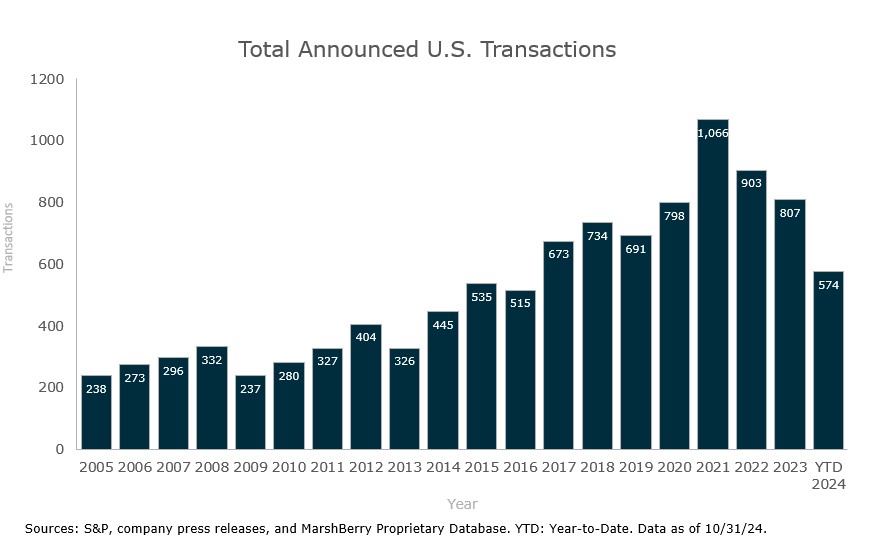

Through October 2024, the U.S. M&A market has witnessed a notable uptick in activity, with 574 announced transactions, reflecting a 5.7% increase from the previous year. Private capital-backed buyers have significantly bolstered this trend, accounting for 73.5% of deals—up from 59.3% in 2019. Independent agencies continue their steady participation, rising slightly to 16.7%.

Conversely, bank-backed acquisitions have dwindled to a historic low of just five deals in 2024, down from 18 in 2022. Specialty distributors remain a primary focus for dealmakers, comprising 15.2% of total deals this year. This shift in market dynamics underscores the evolving landscape of U.S. M&A activity.

On a global scale, corporates are shifting from being net-sellers to net-buyers, a transformation that’s increasingly evident despite challenges like high-interest rates and regulatory unpredictability. Through Q3 2024, corporate buyers accounted for 71% of M&A activity, a marked increase from the 61% share seen in 2021 and 2022. This surge is attributed to pent-up demand, healthy balance sheets, and a drive to realign portfolios through separations and strategic acquisitions.

Yet, a tightening regulatory environment has created bottlenecks, especially for large transactions ($10B+), which now take twice as long to finalize as they did a decade ago. Adding to the slowdown is the tightening grip of monetary policy. With elevated interest rates, the “dimmer switch” effect on corporate M&A has intensified, dampening valuations and raising debt financing costs. This has particularly affected merger arbitrage funds, which have faced longer closing times and more blocked deals. Fundamental shareholders, likewise, have shown a preference for smaller, cash-flow accretive transactions, which provide scale without the associated risk.

That said, the second half of 2024 witnessed an uptick in investor risk appetite. More than half of acquirers outperformed the market post-announcement of their deals, reflecting optimism about future growth. Looking ahead, with expectations that the cost of capital will ease and potential policy shifts are absorbed in 2025, demand for strategic M&A is poised for a resurgence.

With the presidential election behind us, clarity on tax policies for 2025 and beyond is taking shape. President-elect Trump has reaffirmed his intention to extend the Tax Cuts and Jobs Act (TCJA) of 2017, keeping capital gains taxes at current levels or potentially lowering them further. With the likelihood of Republican control over both the Senate and the House, his plans for tax cuts may progress more easily, which could quell fears of capital gains tax hikes.

The 2017 TCJA brought down the corporate tax rate to a flat 21%, but Trump’s proposal now suggests a further reduction to 15% for domestic production. This could spur business exits, as companies may seek to capitalize on favorable tax conditions, with private equity firms poised to acquire undervalued assets, sell them at peak prices, or take them public.

Moreover, recent interest rate cuts from the Federal Reserve—50 basis points in September and 25 in November, with additional reductions expected in 2025—will likely boost borrowing activity. This, in turn, should provide continued opportunities for investment, particularly in sectors like insurance brokerage, where dealmaking is expected to thrive. With these policy shifts in place, 2024 could set the stage for a strong continuation of M&A activity well into 2025.

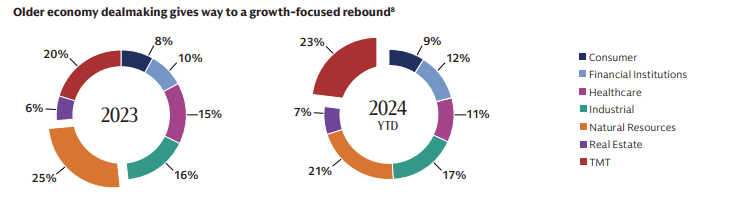

Mergers and acquisitions (M&A) activity in 2024 is showing signs of a strong recovery, following a period of uncertainty characterized by high inflation and geopolitical tensions. Stabilizing macroeconomic conditions, the reopening of financing markets, and growing confidence among corporate boards suggest that global M&A transactions will surge, particularly in energy, technology, and healthcare sectors, which are poised to lead the revival. While high interest rates and regulatory challenges remain, the general outlook is optimistic as deal volumes are expected to rise, reflecting a more focused approach to value creation.

Private equity is also active, particularly in take-private deals. Data from PitchBook reveals 136 take-privates in 2023, up 15% from the previous year. By mid-2024, 97 such deals had already occurred, positioning the industry on track to meet or exceed last year’s volume. The technology sector is notably dominant in these transactions, with 46 of the deals closed in 2024. These include both deals announced in 2023 and those completed or set to close in 2024, highlighting continued momentum despite lingering macroeconomic challenges.

ExxonMobil’s acquisition of Pioneer

Deal value: $59.5 billion.

ExxonMobil completed its acquisition of Pioneer Natural Resources in an all-stock transaction valued at approximately $60 billion. This strategic move has not only significantly expanded ExxonMobil’s presence in the Permian Basin but has also more than doubled its footprint in this prolific oil-producing region.

The merger combined Pioneer’s substantial acreage and expertise with ExxonMobil’s technological capabilities and financial strength, creating an industry-leading position in U.S. unconventional oil and gas resources.

Capital One Financial Corporation’s Acquisition of Discover Financial Services

Deal value: $35 billion.

Capital One Financial Corporation announced its intention to acquire Discover Financial Services in an all-stock transaction valued at $35.3 billion.

Hewlett Packard Enterprise’s Acquisition of Juniper Networks

Deal value: $14 billion.

Hewlett Packard Enterprise’s (HPE) planned $14 billion acquisition of Juniper Networks marks a significant move in the tech industry, aiming to enhance HPE’s position in cloud services and advanced computing. This strategic acquisition will double HPE’s networking business, creating a comprehensive portfolio that offers customers and partners a compelling new choice to drive business value.

IBM Buying HashiCorp for $6.4 Billion

On April 24 IT giant IBM said it had struck a deal to buy HashiCorp, developer of the Terraform “infrastructure-as-code” platform, in a $35-per-share cash deal valued at $6.4 billion.

Nuvei: $6.3 billion

Canadian fintech Nuvei, which provides companies with a range of services spanning payments processing, risk management, currency conversion, and more, entered into an agreement in April to be taken private by Advent International in a deal worth $6.3 billion.

SAP Buys WalkMe for $1.5 Billion

SAP struck a deal in June to buy adoption platform specialist WalkMe in an all-cash, $14-per-share transaction valued at about $1.5 billion. SAP said the acquisition would provide a boost to its Signavio, LeanIX and generative AI offerings including its Joule copilot.

Nvidia Buys Run.ai For $700M In AI Infrastructure Play

In April AI chip leader Nvidia sought to maintain its momentum in the artificial intelligence hardware space by purchasing AI infrastructure management startup Run.ai for $700 million.

Prior to 2025 two mega potential mega mergers were announced to be in talks and could have major ramifications on the global economy:

In an unexpected move that could alter the global automotive sector, Japanese car manufacturers Nissan, Honda, and Mitsubishi have confirmed they are in discussions for a potential three-way merger. If successful, this unprecedented collaboration would unite Japan’s second- and third-largest carmakers, Nissan and Honda, alongside Mitsubishi, forming a formidable force in the automotive industry. With this merger, the trio would become the world’s third-largest carmaker by annual sales, trailing only Toyota and Volkswagen. This strategic alliance would strengthen their position amid increasing market pressures and rapid technological changes.

Quebec’s Alimentation Couche-Tard, a company that began with a single store in 1980, is now poised to become a major global player, with plans to potentially acquire the world’s largest convenience store operator, 7-Eleven. 7-Eleven’s 84,000 stores worldwide are currently owned by the Japanese giant, Seven & i Holdings, which recently turned down a $38.5 billion bid from Couche-Tard. However, the Canadian company is reportedly considering raising its offer, leaving the door open for a future deal that could reshape the global retail landscape.

The potential acquisition has stirred a range of reactions. Japanese consumers are apprehensive about the possibility of their beloved 7-Eleven stores being altered by a foreign owner, fearing changes to the stores’ cultural identity. In the U.S., there is concern that the acquisition might disrupt plans for expanding Japanese-inspired products in American locations. Meanwhile, Canadians are watching eagerly to see if this could lead to an improved experience at their local 7-Elevens, possibly offering enhanced offerings or store upgrades.

This deal has all the makings of a significant shift in the global retail and convenience store sectors. With the strategic vision of Couche-Tard’s leadership, an acquisition of 7-Eleven would elevate the company to a new echelon, potentially becoming one of the largest and most influential retailers in the world. How this story unfolds will have ramifications not only for the companies involved but also for the millions of customers who frequent these stores daily, from the bustling streets of Tokyo to suburban North America.

What we expect/Predict for M&A for 2025

Mergers and acquisitions (M&A) activity in 2025 is expected to be shaped by multiple trends. One notable shift is the anticipated increase in smaller deals, especially in sectors such as publishing, where mid-sized companies face financial pressure due to inflation and heightened competition. We foresee major publishers like Penguin Random House and Simon & Schuster capitalizing on this by acquiring smaller entities to bolster their portfolios.

In the technology sector, M&A activity is projected to rebound following a relatively slow 2023, with firms particularly eager to engage in smaller acquisitions within high-growth fields such as artificial intelligence (AI) and cybersecurity. Despite challenges posed by high interest rates and regulatory scrutiny, the demand for strategic, value-enhancing acquisitions remains robust. Private equity firms, flush with record levels of capital, are poised to capitalize on these opportunities.

Consolidation within the healthcare industry is also expected to accelerate as hospitals and health systems look to scale and diversify services, particularly in outpatient care and mental health. Driven by financial distress and labor challenges, M&A will be a lifeline for many hospitals aiming to survive and thrive amidst ongoing pressures. Larger health systems are positioning themselves to expand both their offerings and geographical reach through acquisitions.

However, there are significant challenges on the horizon. Despite optimism surrounding M&A activity, financing remains expensive and valuations lower than during the boom years of 2020 and 2021. Dealmakers will need to be more creative to generate the returns seen in those high-growth years. Regulatory pressures, particularly in sensitive areas such as AI and cross-border transactions, may continue to slow deal timelines and create uncertainty, making it necessary for companies to adjust their strategies accordingly.

Looking beyond these hurdles, the second half of 2024 and into 2025 is expected to witness a growing appetite for M&A activity. Technology-driven deals, especially in AI, machine learning, and other cutting-edge technologies, will likely take center stage. Moreover, cross-border M&A will rise as companies strive to secure their supply chains, expand market reach, and tap into global opportunities. Regulatory oversight in these transactions, particularly in AI and other strategic sectors, could add complexity to the deal-making process, but companies will adapt their strategies to meet evolving demands.

Ultimately, the M&A landscape for 2025 promises to be dynamic, with a strong focus on smaller, strategic acquisitions as businesses adapt to a changing economic and regulatory environment. While financing conditions will remain challenging, the underlying demand for expansion and diversification will fuel continued deal volume, with tech and healthcare sectors leading the charge. The evolution of cross-border M&A and regulatory compliance will further shape the industry’s trajectory, making 2025 a year of calculated, strategic acquisitions across industries.

Companies on our M&A Radar

In the evolving world of M&A, Lyft emerges as a prime target for acquisition, with Amazon being a likely suitor. The ride-hailing platform’s 24 million active users make it an attractive prospect, especially as Amazon seeks to leverage its Zoox autonomous vehicle technology. This strategic acquisition could provide Amazon with a significant edge in the race to dominate the robotaxi market, competing head-to-head with Tesla and Waymo.

Beyond ride-hailing, the tie-up could propel Amazon deeper into food delivery, expanding its reach in critical logistics. Lyft’s infrastructure serves as an ideal foundation for scaling Zoox’s autonomous capabilities, turning it into a crucial asset in reshaping transportation. The market response has been positive, with Lyft shares rising significantly, reflecting investor optimism about the potential acquisition.

For Amazon, this isn’t just about securing a foothold in mobility; it’s about securing the future of both passenger and goods transportation. By acquiring Lyft, Amazon would position itself as a major player in the autonomous revolution, reshaping how goods and people move in a rapidly transforming world.

If the deal goes through, it would force competitors like Uber to reassess their strategies and potentially set a new precedent for the industry. Whether or not the merger materializes, it signals Amazon’s intent to take a leading role in autonomous vehicles, underscoring its broader vision of dominating future transportation networks. Investors would be wise to keep their eyes on this space, as the potential ripple effects of such a move would undoubtedly shake up the sector for years to come.

nCino, a North Carolina-based fintech, is once again finding itself at the center of acquisition speculation, particularly as its stock price remains about half of what it was in the previous year.

After being rumored for a potential privatization in 2023, many analysts believe the company is once again a prime target for a deal, with the momentum for M&A gathering speed. The company’s board has reportedly been discussing a special committee to evaluate offers.

The firm, which provides cloud banking solutions, has worked with more than 1,850 financial enterprises, positioning it as an attractive asset in the growing digital banking space. Despite Insight Partners’ sizable stake, it’s unclear whether they will remain involved or cash out.

Additionally, nCino’s presence in areas such as loan origination and banking compliance further enhances its value as a potential acquisition target. With the increasing interest in fintech and the broader trend of private equity firms snapping up related companies, nCino’s future in the M&A space could very well be on the horizon. Given the wider momentum within the sector and the company’s strategic position in the market, 2025 could be the year where this ongoing speculation comes to fruition.

With 2025 here industry watchers are eyeing Hollywood and Wall Street for the next wave of mergers and acquisitions, particularly with the potential changes under a Trump administration. Among the names in play are Lionsgate, AMC Networks, and Roku, all of which are considered ripe for acquisition. Lionsgate, in particular, stands out due to its relatively low market valuation, coupled with its strong portfolio of content and intellectual property. Insider buying activity further fuels speculation that a potential buyout may be on the horizon, with 2025 being a prime year for such a move.

Laurentian Bank, a relatively smaller player in the Canadian banking sector, is widely expected to be involved in mergers and acquisitions (M&A) in 2025, though likely as the target rather than the acquirer.

With its larger competitors—the Big Six—holding dominant market shares and Systemically Important Bank (SIB) status, Laurentian has found it difficult to compete. Consequently, the bank is actively seeking a buyer. While no acquisition materialized in 2024, analysts predict that one of the large banks will make a move next year.

Laurentian’s financial position shows strengths in liquidity, with cash holdings of $8.3 billion, but its $17.9 billion debt load and ongoing challenges in key business areas suggest that a strategic sale could be the best option for its future.