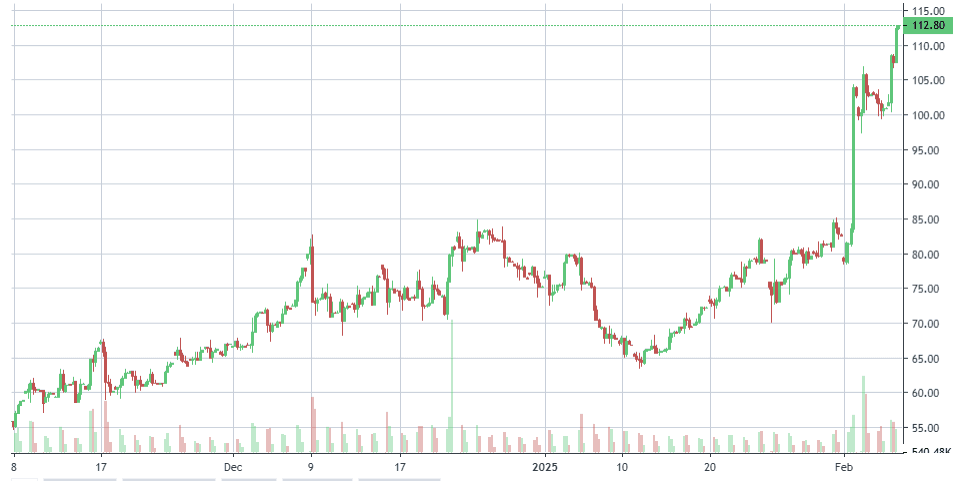

Palantir Technologies, the once-shadowy purveyor of data analytics and artificial intelligence, has become a market spectacle. In a rally that seems to defy gravity, its shares have surged 38% in just five days, extending an extraordinary 62% gain since our initial sell recommendation—a rare instance where trimming exposure in a red-hot stock leaves one feeling both prudent and premature.

On Thursday, Palantir shares vaulted another 10%, closing at a record $111.28, cementing its place as one of the best-performing stocks in the Nasdaq 100 and S&P 500. The earnings-induced euphoria has propelled the company’s market capitalization to an astonishing $240 billion, surpassing venerable institutions like American Express ($221 billion), McDonald’s ($208 billion), and Disney ($207 billion)—companies with balance sheets built on tangible assets rather than algorithmic clairvoyance.

With this ascent, Palantir has joined the exalted ranks of America’s 47 “mega-cap” stocks, those valued above $200 billion. A stunning feat for a firm that once operated at the periphery of Wall Street’s imagination—now firmly at its center, a testament to the unrelenting appetite for all things AI.

Palantir Technologies has staged an extraordinary rise, its stock now more than tenfold its value from just two years ago, when its market capitalization languished below $20 billion. In 2024, the company derived 55% of its revenue from government contracts, cementing its position as an indispensable partner in the age of AI-driven defense and intelligence. Its clientele includes names as varied as Amazon and the Department of Defense, a juxtaposition that speaks to its broad yet highly specialized appeal.

Crowning its triumph, Palantir was the best-performing stock in the S&P 500 in 2024, and its momentum shows little sign of abating—rising 40% already in 2025. Yet, such parabolic gains bring with them an equally steep valuation. By the oft-invoked price-to-sales metric, Palantir is the most expensive stock in the S&P 500, trading at 70 times revenue—an Olympian altitude that dwarfs both the S&P 500 average of 3 and even the 35 times sales multiple of AI juggernaut Nvidia.

The crucial question: Can Palantir keep surpassing expectations? The answer likely hinges on its ability to harness AI to further entrench itself within both commercial enterprises and government agencies. Historically regarded as a creature of the defense establishment, Palantir has more recently expanded its reach into the private sector, benefiting from the fervent adoption of its AI platform across both domains.

Intriguingly, the company sees opportunity in federal budget cuts imposed by the newly christened Department of Government Efficiency, helmed by Elon Musk—a development Palantir’s Chief Technology Officer, Shyam Sankar, spun as a competitive advantage on the firm’s February 3 investor call. “Palantir’s real competition is a lack of accountability in government,” he quipped, positioning the company as an enforcer of operational rigor amid bureaucratic belt-tightening.

Despite the stock’s all-time highs, prudence dictates restraint. We maintain a Sell/Hold stance, recognizing that valuations this stretched seldom escape the eventual force of gravity. While a further rally toward $145 by year-end is conceivable, we would not be shocked to see the stock retreat to the $50–$40 range should broader market conditions sour or should Palantir encounter an impassable hurdle. We have won handsomely here; now is not the time for excessive greed.

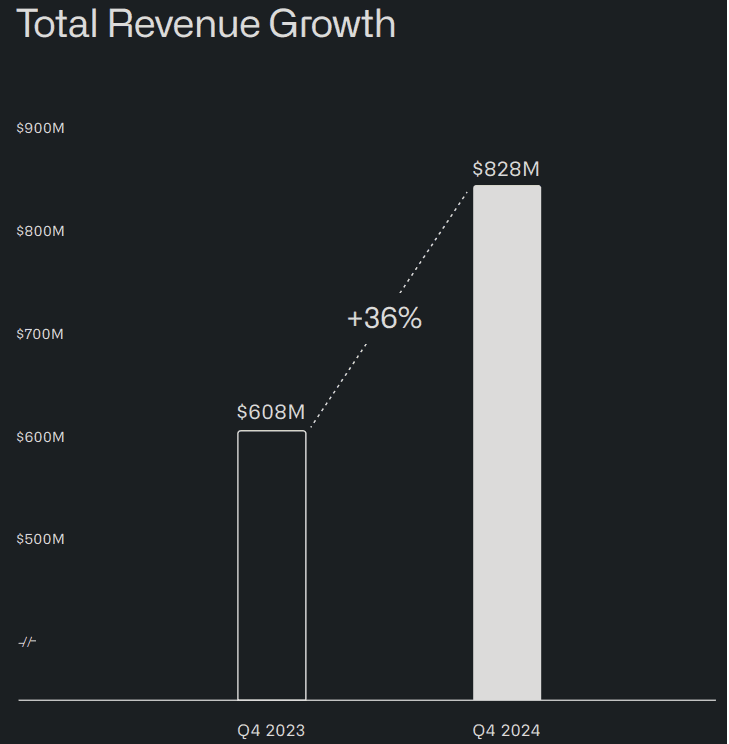

Palantir’s fourth-quarter revenues soared to $828 million, marking a 36% year-over-year increase and surpassing analyst expectations by $52 million, per London Stock Exchange Group (LSEG) estimates. The company’s adjusted earnings per share landed at 14 cents, exceeding consensus projections by three cents—a modest but meaningful margin in an era where expectations are finely calibrated.

The forward guidance was equally striking. First-quarter 2025 revenue is projected at $860 million—the midpoint of Palantir’s range, yet a figure that exceeds analyst estimates by $61 million. The full-year outlook was even more ambitious, with 2025 revenue forecasted at $3.75 billion, outpacing LSEG’s estimate by $230 million.

Breaking down the numbers:

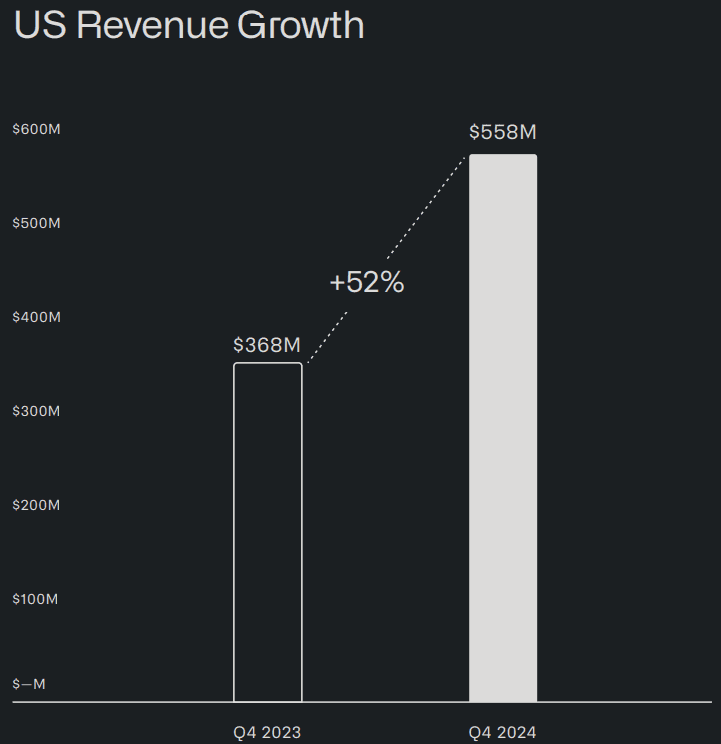

U.S. revenue surged 52% year-over-year and 12% quarter-over-quarter to $558 million

U.S. commercial revenue climbed 64% year-over-year and 20% quarter-over-quarter to $214 million

U.S. government revenue expanded 45% year-over-year and 7% quarter-over-quarter to $343 million

Overall revenue grew 36% year-over-year and 14% sequentially to $828 million

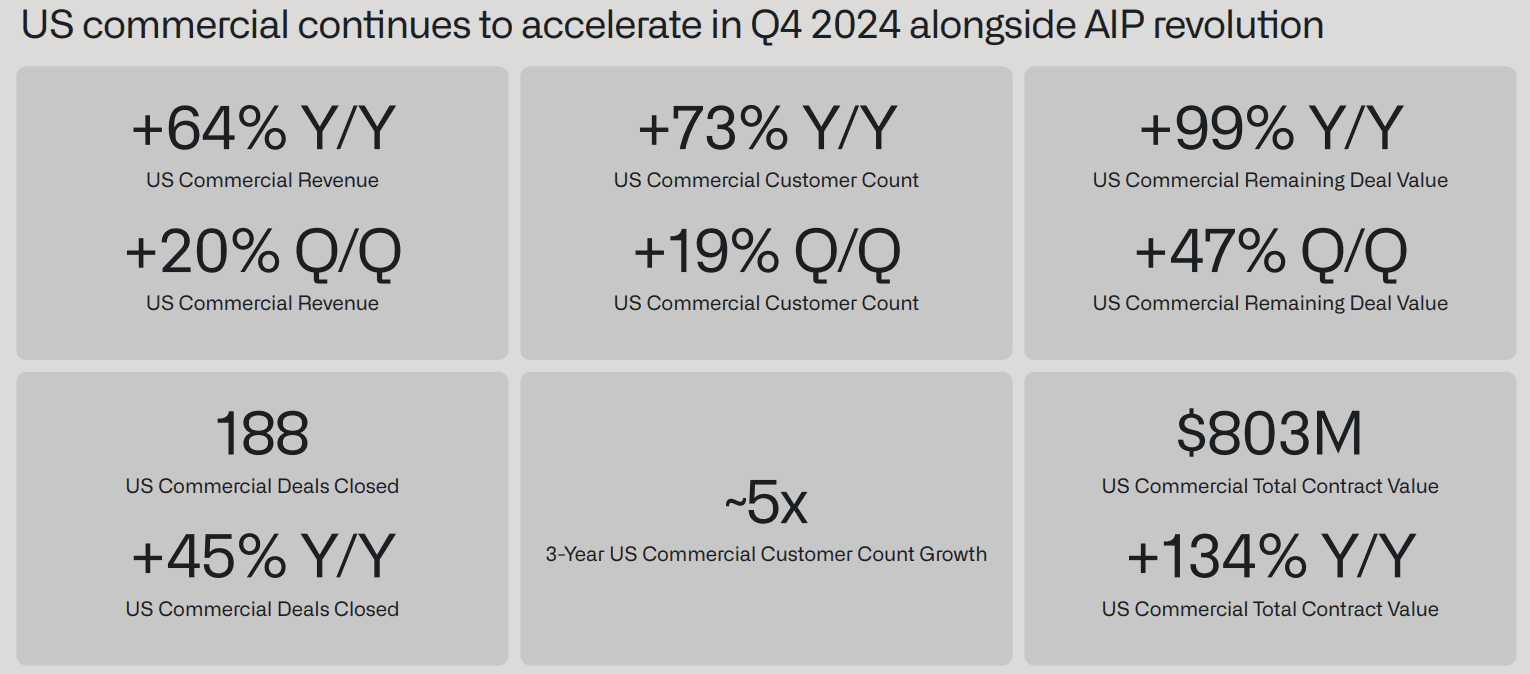

Palantir’s deal-making prowess was equally formidable. The firm closed 129 contracts worth at least $1 million, alongside 58 deals exceeding $5 million and 32 surpassing $10 million. But perhaps the most staggering statistic was its record-setting $803 million in U.S. commercial total contract value (TCV)—a 134% year-over-year surge and a 170% sequential jump.

On a broader scale, Palantir’s remaining deal value (RDV) in U.S. commercial operations swelled to $1.79 billion, reflecting a 99% year-over-year gain and a 47% quarter-over-quarter rise.

The numbers tell a tale of explosive expansion—but the market’s infatuation with Palantir’s growth may yet meet the sobering arithmetic of valuation. For now, the company continues to defy expectations. The question remains: Can it continue to outrun them?

Palantir Technologies, an undisputed leader in artificial intelligence and data analytics, continues to solidify its position as a linchpin in the global defense and intelligence sectors. Its technology is deeply embedded in U.S. government operations, with the company counting all branches of the U.S. military as clients, as well as American allies in Ukraine and Israel.

The firm’s AI platform, AIP, plays a central role in enabling clients to synthesize disparate data sources into unified models—models that can then be trained, refined, and deployed to enhance day-to-day decision-making. The demand for Palantir’s AI capabilities is accelerating, evidenced by a recent expansion of its contract with the U.S. Army, which could reach $619 million by 2028, in addition to an extension of AI work with U.S. Special Operations Command.

Moreover, Palantir’s ontology service—a tool that connects data, entities, and processes—has proven indispensable to its commercial clients and is witnessing a surge in demand. The company’s strategic vision is clear: to replace traditional defense contractors with software-first solutions, an ambition it is advancing through enhanced collaborations. Most notably, Palantir has deepened its partnership with weapons-maker Anduril Industries, further positioning itself at the crossroads of AI and defense.

In a noteworthy move, Palantir has also entered into a new alliance with AI startup Anthropic to introduce large language models into U.S. intelligence and defense operations.

The fourth-quarter 2024 results from the company reflect a continued momentum in both growth and profitability.

Customer Growth:

The customer base expanded by a notable 43% year-over-year and 13% quarter-over-quarter, underscoring the growing demand for its services.Cash from Operations: Strong operational efficiency yielded $460 million in cash from operations, translating to a 56% margin.Free Cash Flow: Adjusted free cash flow reached $517 million, with an impressive 63% margin, illustrating the company’s capacity to generate cash efficiently.

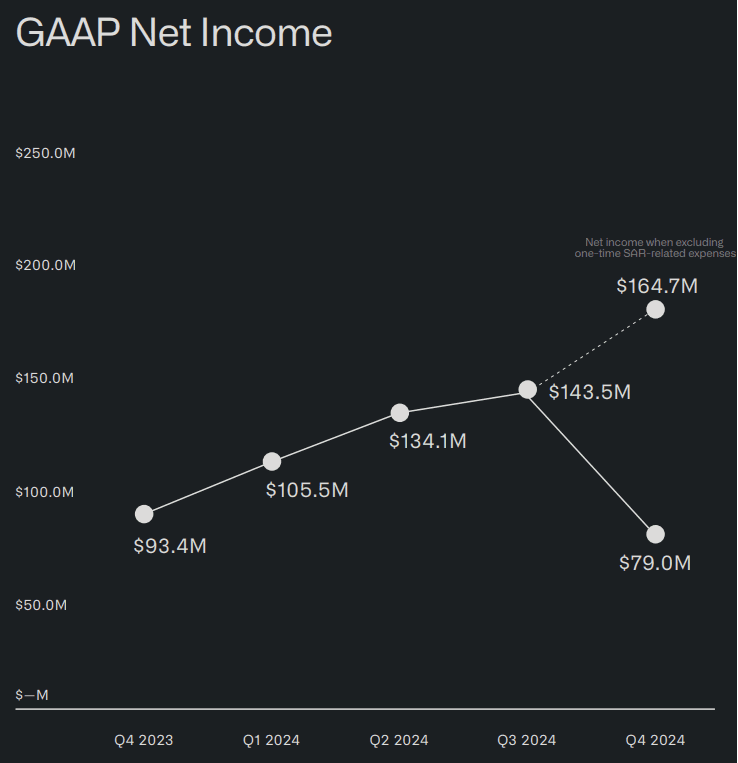

Net Income:

The company reported a GAAP net income of $79 million, a solid 10% margin, though this figure was impacted by one-time expenses. Excluding these SAR-related costs, net income surged to $165 million, reflecting a healthier 20% margin.

Income from Operations: GAAP income from operations stood at $11 million, representing a slim 1% margin, though excluding one-time expenses, this increased to $142 million, yielding a much stronger 17% margin. The adjusted income from operations was even more robust, coming in at $373 million, with a substantial 45% margin.

Efficiency Score:

The company posted an impressive Rule of 40 score of 81%, signaling both high growth and profitability.

Earnings Per Share (EPS): GAAP EPS was $0.03, with adjusted EPS coming in at $0.14, further highlighting the company’s ability to grow earnings amid a challenging market environment.

Liquidity Position: The firm ended the quarter with $5.2 billion in cash, cash equivalents, and short-term U.S. Treasury securities, ensuring ample liquidity for future growth and investment.

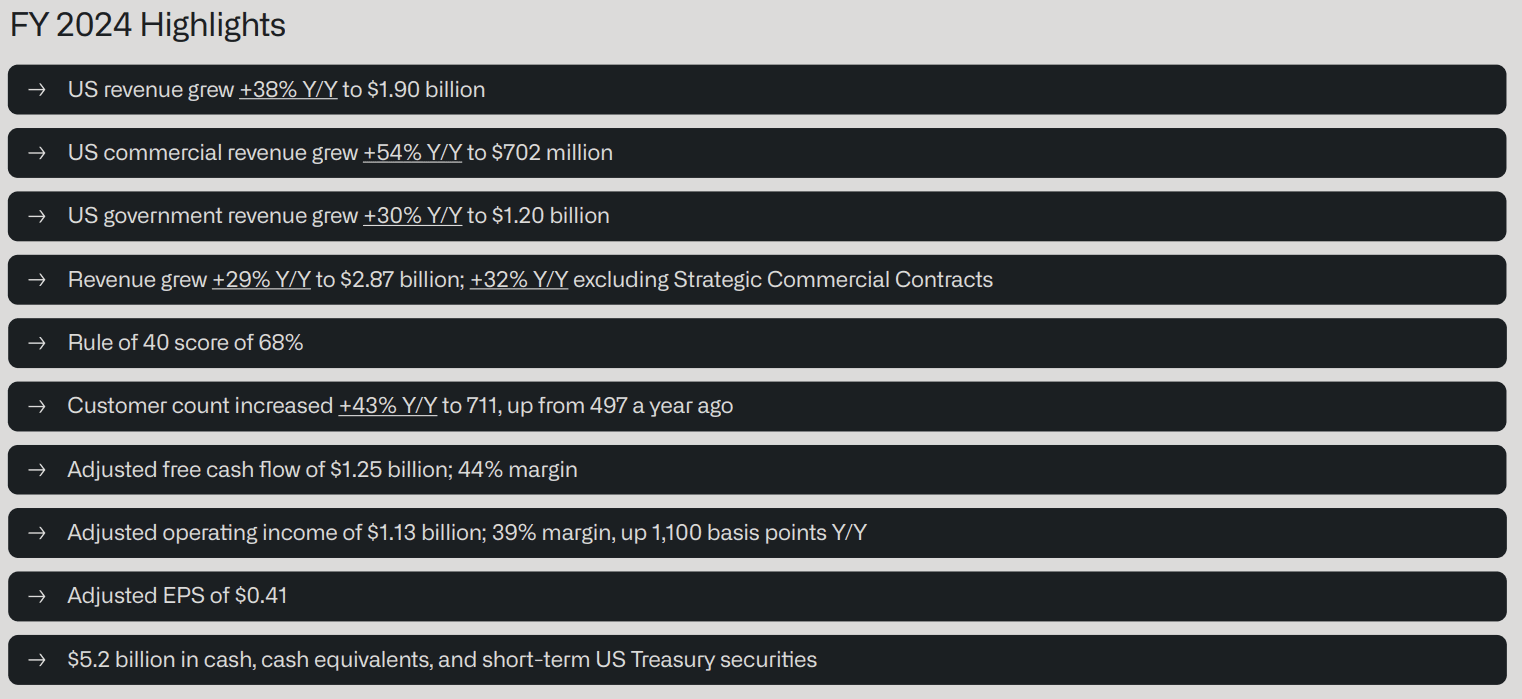

The full-year results for 2024 demonstrate a notable trajectory of growth, profitability, and operational efficiency across key segments.

U.S. Revenue Growth: The U.S. business experienced a 38% year-over-year increase, reaching $1.90 billion, driven by robust demand in both commercial and government sectors.

U.S. Commercial Revenue: This segment surged 54% year-over-year, totaling $702 million, highlighting significant commercial expansion.

U.S. Government Revenue: U.S. government revenue rose 30% year-over-year to $1.20 billion, underscoring strong demand within the public sector.Overall Revenue: Total revenue for the year grew by 29% year-over-year to $2.87 billion, reflecting a healthy top-line expansion.

Cash Flow and Operational Efficiency:

Cash from operations amounted to $1.15 billion, yielding a strong 40% margin.

Adjusted free cash flow reached $1.25 billion, with a solid 44% margin, signaling excellent cash generation and operational control.

Profitability Metrics:

GAAP net income stood at $462 million, a 16% margin, reflecting healthy bottom-line growth despite one-time costs.

GAAP income from operations came to $310 million, representing an 11% margin. However, excluding SAR-related one-time expenses, this figure improved to $442 million, yielding a 15% margin.

Adjusted income from operations reached $1.13 billion, with a robust 39% margin, indicating strong ongoing operational performance.

Overall, FY 2024 results reflect a balanced mix of revenue growth, margin expansion, and financial discipline, positioning the company well for continued success in 2025.

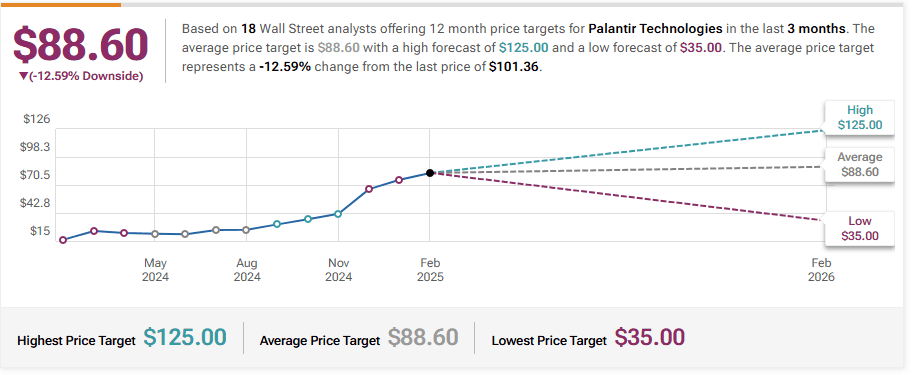

Citigroup Maintains Neutral on Palantir Technologies, Raises Price Target to $110

RBC Capital Maintains Underperform on Palantir Technologies, Raises Price Target to $40

UBS Maintains Neutral on Palantir Technologies, Raises Price Target to $105

DA Davidson Maintains Neutral on Palantir Technologies, Raises Price Target to $105

Cantor Fitzgerald Maintains Neutral on Palantir Technologies, Raises Price Target to $98

Baird Maintains Neutral on Palantir Technologies, Raises Price Target to $100

B of A Securities Maintains Buy on Palantir Technologies, Raises Price Target to $125