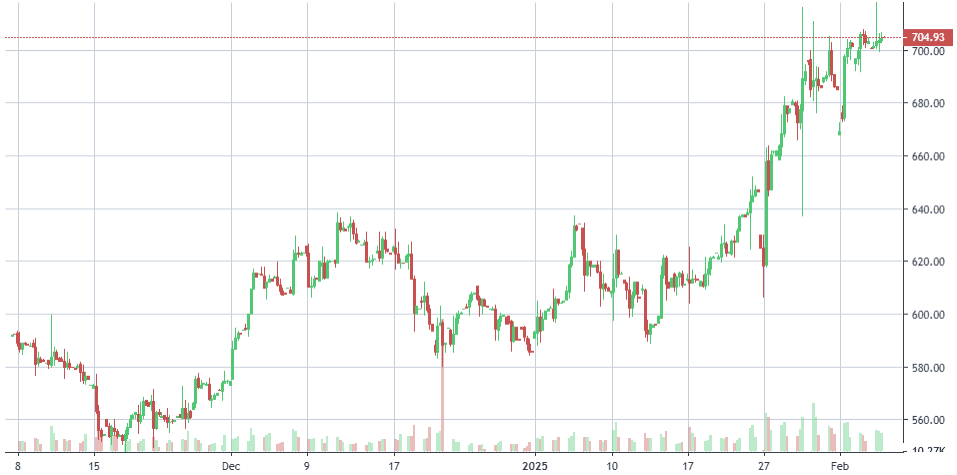

January proved to be a month of triumph for Meta Platforms, as the social media colossus surged ahead while much of the tech sector floundered. A convergence of political, regulatory, and technological tailwinds propelled the stock upward, culminating in an 18% gain for the month, according to S&P Global Market Intelligence.

Meta’s ascent began with speculation over a potential TikTok ban—a political chess move that, however fleeting in duration, underscored the regulatory uncertainties plaguing its Chinese rival. The inauguration of President Donald Trump further buoyed sentiment, with investors sensing a newfound alignment between Meta’s interests and the administration’s regulatory posture.

Then came the AI shake-up. The late-January unveiling of DeepSeek sent shockwaves through the artificial intelligence sector, battering many AI-adjacent stocks. Yet Meta stood apart. Instead of recoiling, the company’s open-source doctrine found validation. CEO Mark Zuckerberg, ever the pragmatist, acknowledged DeepSeek’s innovations with measured admiration, remarking that Meta was already considering integrating some of its novel techniques.

More significantly, Zuckerberg framed DeepSeek’s emergence as a vindication of Meta’s decision to open-source its own large language model, Llama. “There’s going to be an open-source standard globally,” he declared, adding that it was “important that it’s an American standard.” The implicit message? In a world where AI dominance is increasingly a geopolitical contest, Meta’s strategy positions it at the helm of a Western-led paradigm.

If regulatory and AI tailwinds weren’t enough, Meta delivered yet another catalyst in the form of blockbuster fourth-quarter earnings. Investors responded with enthusiasm, sending the stock sharply higher in the final days of January.

For all the tempest surrounding the tech sector, Meta stands not as a casualty but as a kingmaker—adept at navigating political crosscurrents, capitalizing on AI’s tectonic shifts, and delivering financial performance that reaffirms its dominance.

Emerging from a triumphant 2024, Meta Platforms finds itself in a position of formidable strength. Its stock has soared, its quarterly results have dazzled, and it now presides over the most widely used AI assistant, Meta AI. In an era where artificial intelligence defines competitive moats, Meta has sharpened its own with remarkable precision.

Investors, emboldened by the company’s momentum, wagered that January would bring further gains, and for good reason. The social media titan is primed to reap the rewards of industry-wide shifts, from AI-powered advertising to content curation. Even so, valuation concerns linger in the wake of recent rallies. For those with a measured disposition, an initial entry point in the $520-$550 range seems prudent, with reserves kept aside should the stock retreat.

Challenges persist, of course. The company’s breakneck AI expansion demands significant capital expenditure, which, in turn, applies near-term pressure to margins. Yet the broader trajectory remains unmistakable: Meta’s ability to fuse AI with its advertising machinery strengthens its long-term growth calculus. Indeed, its ad-driven revenue model—already among the most sophisticated in the world—appears increasingly adept at monetizing its ever-expanding digital empire.

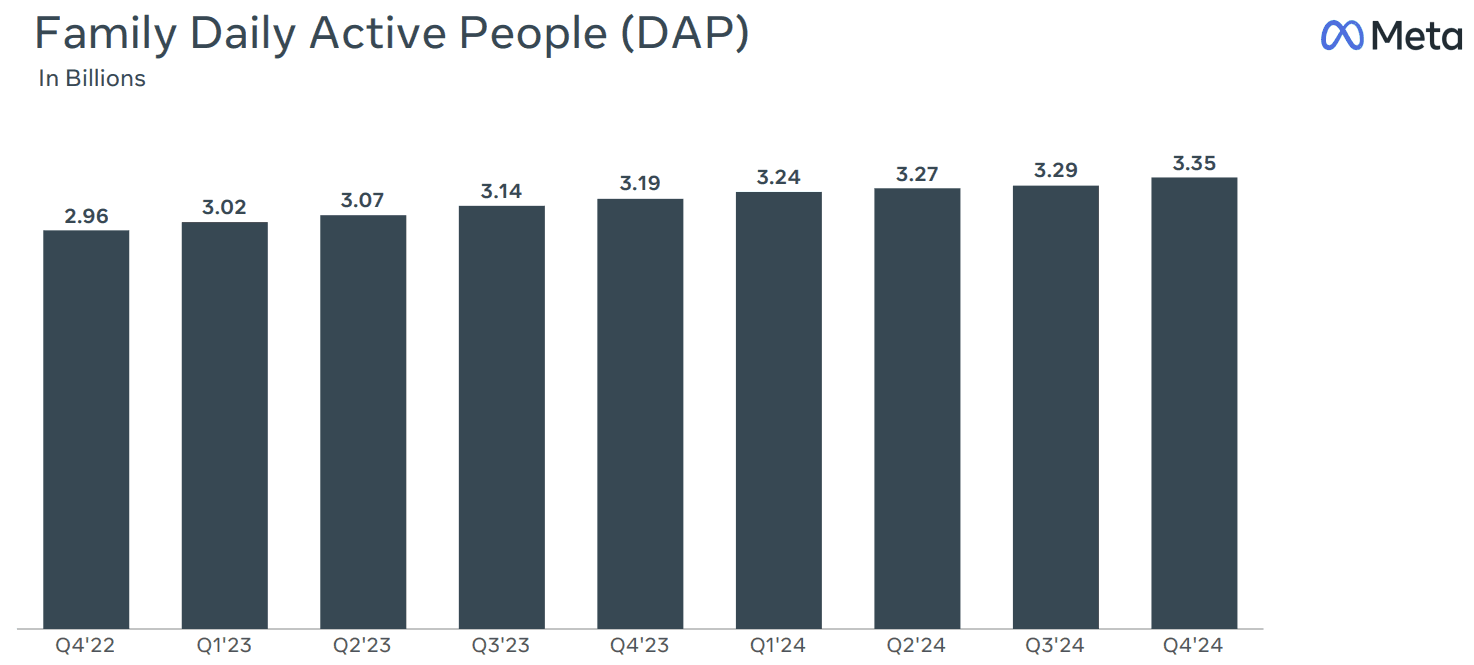

The numbers tell the tale. Global user growth ticked up another 5% year over year, reaching a staggering 3.35 billion. More critically, Meta has found ways to extract more value from each user, with average revenue per user rising 16%—an impressive feat for a company of its scale.

Against this backdrop, we recalibrate our fair value estimate for Meta upward, from $590 to $770. This reassessment stems largely from an increasingly optimistic outlook on Meta’s AI monetization strategy, which is already yielding tangible results. More than 4 million advertisers now employ its generative AI tools to craft campaigns—a fourfold increase in just six months. Meanwhile, AI-powered ad ranking systems continue to refine personalization, enhancing both engagement and revenue efficiency.

Artificial intelligence may be the future, but it is proving to be an exceedingly expensive one. Meta, Google, Microsoft, and Amazon have each signaled their intent to spend lavishly, collectively earmarking no less than $315 billion in capital expenditures for 2025—an overwhelming share of which is devoted to AI.

Meta, for its part, has outlined an ambitious budget ranging from $60 billion to $65 billion, while Google’s parent, Alphabet, intends to deploy $75 billion, largely to fortify its data centers, servers, and networking infrastructure. Amazon leads the spending spree with a staggering $100 billion forecasted for the year, trailed by Microsoft at $80 billion, much of which will fuel AI model training and cloud-based AI applications.

Mark Zuckerberg, undeterred by the sheer scale of the investment, regards these outlays not as indulgences but as necessities. His wager is twofold: first, that this unprecedented infrastructure buildout will yield a formidable return on investment, and second, that it will ultimately render Meta a leaner, more efficient enterprise, with AI automation trimming operational expenses.

The vision extends beyond mere infrastructure. On Meta’s recent earnings call, Zuckerberg projected that Meta AI would become the first AI assistant to surpass 1 billion users by year’s end—a milestone that, if realized, would cement its dominance in the space. Meanwhile, green shoots have emerged in other corners of Meta’s ecosystem, including its Ray-Ban smart glasses, which sold over 1 million units in 2024.

A decade ago, such sums devoted to capital expenditures would have raised eyebrows. Today, they barely induce a shrug. In the AI arms race, spending restraint is a luxury no titan can afford.

Reality Labs, Meta’s high-stakes wager on the metaverse, remains a vortex of capital consumption.

Tasked with developing augmented and virtual reality hardware—including Meta Quest headsets and Ray-Ban smart glasses—this division epitomizes the company’s commitment to a digital frontier that has yet to prove its commercial viability.

The price of this ambition? A staggering $17.7 billion in operating losses last year against a meager $2.15 billion in revenue.

Yet, for all the red ink, Mark Zuckerberg remains unwavering. Having rechristened Facebook as Meta in 2021 to signal a full-throated embrace of the metaverse, he now faces a moment of reckoning. Internally, there are signs of mounting urgency. Chief Technology Officer Andrew Bosworth has framed 2024 as the year that will determine whether Reality Labs is a triumph of vision or a cautionary tale of overreach. “We need to drive sales, retention, and engagement across the board, but especially in mixed reality,” he warned in a memo to employees.

Horizon Worlds, Meta’s immersive virtual world, is a particular pressure point. Bosworth conceded that its mobile expansion “absolutely has to break out” if the company’s long-term metaverse ambitions are to remain viable. The problem, of course, is the hardware: bulky, cumbersome headsets that stand as formidable barriers to mainstream adoption.

On Meta’s January 29 earnings call, Zuckerberg acknowledged that 2025 would be a “pivotal year for the metaverse,” admitting that by year’s end, the company will have a clearer sense of whether Horizon’s trajectory is sustainable. For now, Reality Labs remains a costly experiment—a venture bet on a future that may yet arrive, but at an uncertain timeline and an eye-watering expense.

Meta closed 2024 with a flourish, reporting robust growth across key metrics while doubling down on its AI-driven future. The company’s sprawling digital empire saw daily active users (DAP) reach 3.35 billion in December, marking a 5% year-over-year increase.

Advertisers took notice, with ad impressions rising 6% in Q4 and 11% for the full year, while the average price per ad climbed 14% and 10%, respectively—a testament to the platform’s ability to extract greater value from its vast user base.

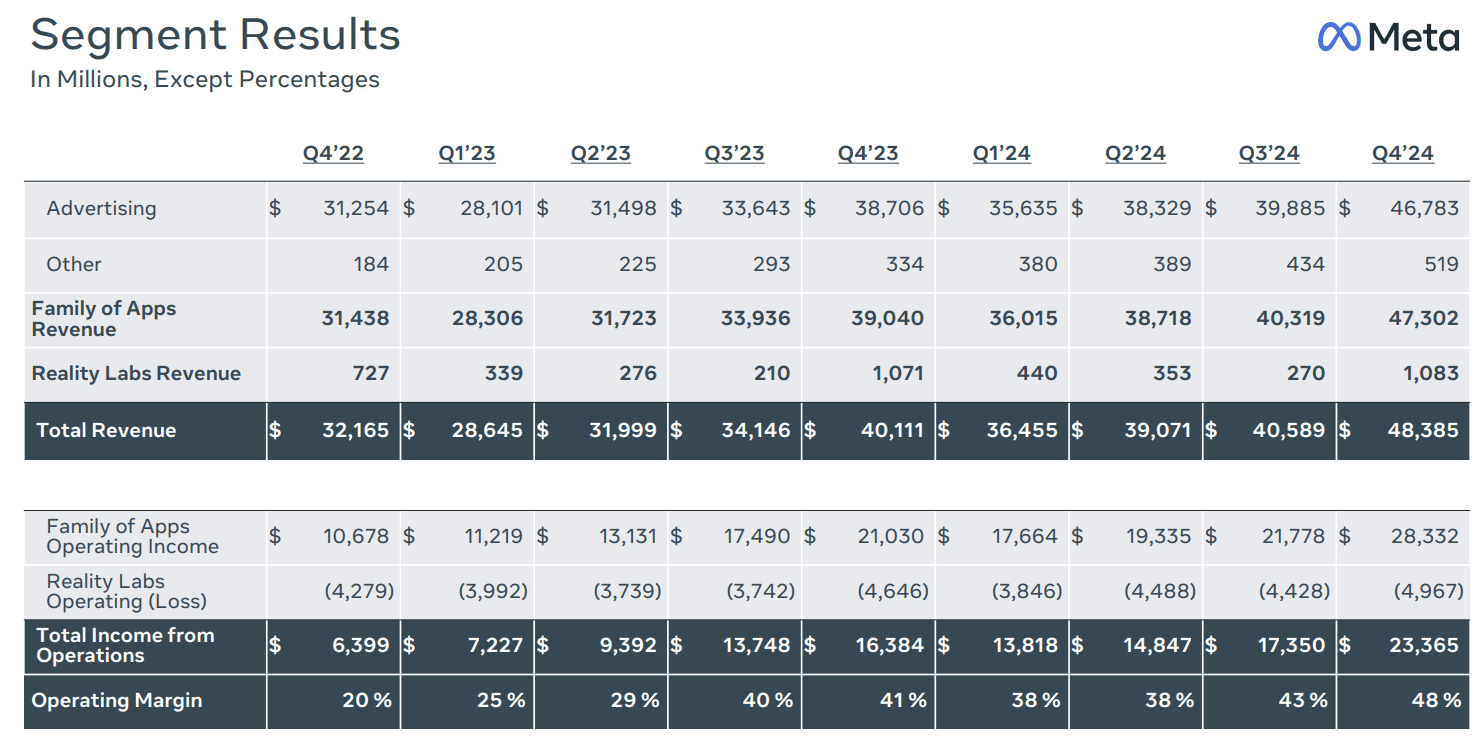

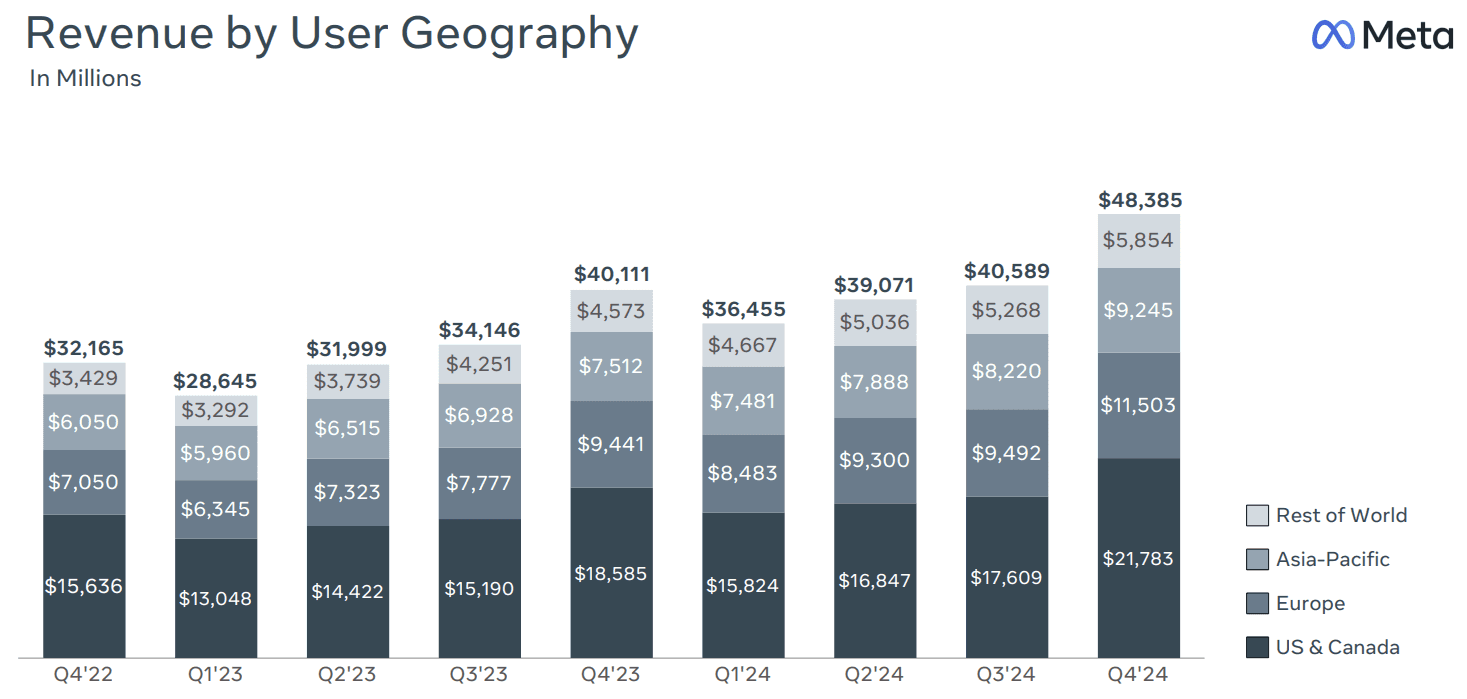

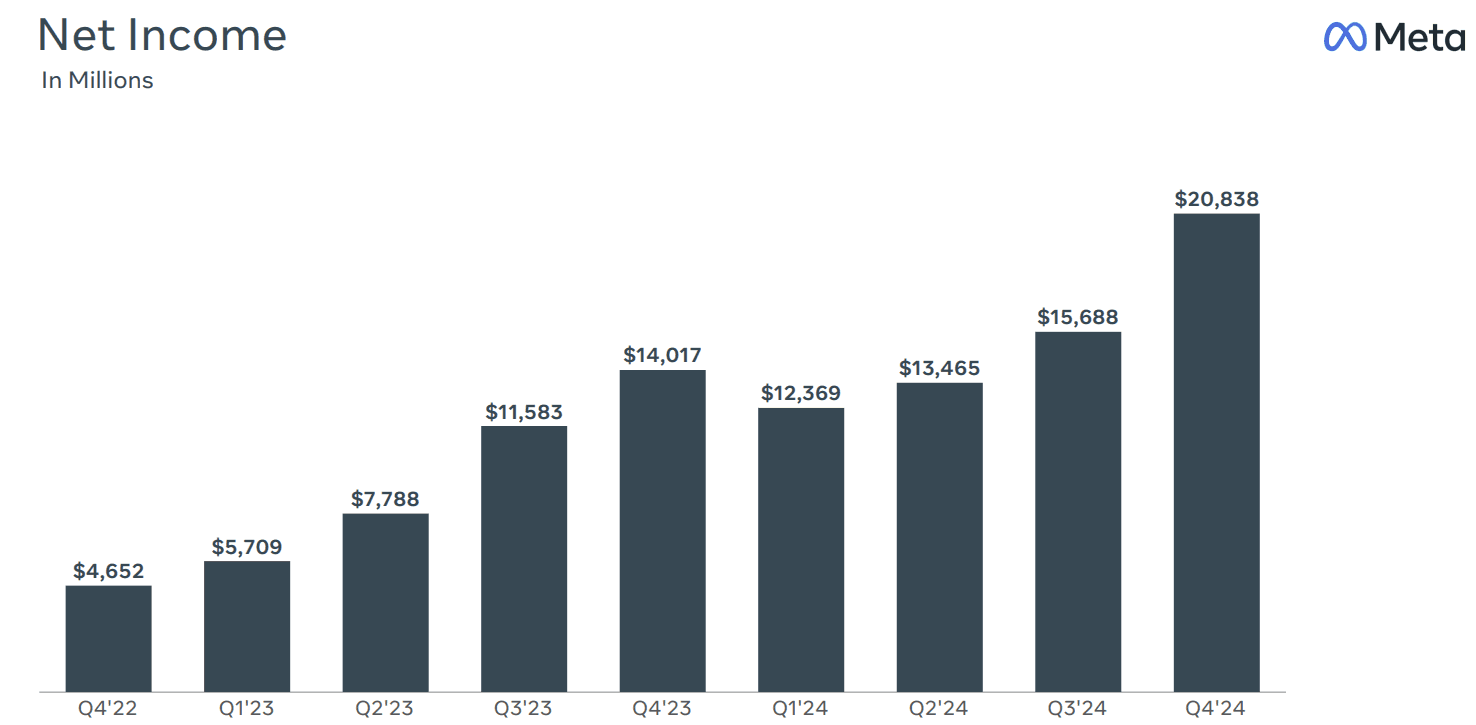

This momentum translated into $48.39 billion in Q4 revenue, up 21% year-over-year, with full-year revenue surging 22% to $164.50 billion. Even stripping out currency fluctuations, growth remained impressive at 21% and 23%, respectively.

Yet, the cost of this expansion was formidable. Total expenses reached $95.12 billion for the year, rising 8% as Meta plowed resources into its ever-expanding digital and AI ambitions. Capital expenditures were no small matter either—$39.23 billion for the year, reflecting Mark Zuckerberg’s enduring belief that an infrastructure arms race will separate the winners from the also-rans. “I continue to think that investing very heavily in CapEx and infra is going to be a strategic advantage over time,” he assured analysts.

Meanwhile, Meta sat on $77.81 billion in cash, cash equivalents, and marketable securities at year’s end, a war chest large enough to withstand the shifting sands of technological disruption. The company’s free cash flow was a formidable $52.10 billion, giving it ample means to fund both its AI aspirations and shareholder returns. Indeed, while stock buybacks were absent in Q4, Meta repurchased $29.75 billion in shares across the year and dispensed $5.07 billion in total dividends.

Meta’s headcount swelled 10% to 74,067 employees, an expansion that underscores the company’s relentless pursuit of AI dominance. And while long-term debt stood at $28.83 billion, it remains a manageable footnote in the face of Meta’s financial firepower.

As 2025 unfolds, the central question remains: Will Meta’s colossal investment in AI—potentially hitting $65 billion this year—become the defining moat Zuckerberg envisions? Investors, for now, appear willing to watch, wait, and wager.

Meta Platforms, an empire built on social connectivity, operates through two distinct yet interwoven domains: Family of Apps (FoA) and Reality Labs (RL).

While the company’s name conjures images of scrolling feeds and viral content, its ambitions extend well beyond the confines of social media, plunging deep into artificial intelligence, virtual reality, and the uncharted frontiers of digital interaction.

The Family of Apps segment remains Meta’s golden goose, encompassing Facebook, Messenger, Instagram, Threads, and WhatsApp—platforms that together form the backbone of its economic machine. This division alone accounts for a staggering 97% of the company’s revenue, an empire of advertising built upon an unassailable fortress of user engagement. Meta’s ad business, refined to near-perfection through sophisticated machine learning algorithms, remains the envy of the industry, deftly monetizing an audience that now boasts 3.35 billion daily active users as of Q4 2024.

Yet, despite regulatory headwinds and intensifying competition, Meta’s advertising juggernaut persists, churning out profits with mechanical efficiency. The company’s unmatched ability to harvest user data and refine its ad targeting ensures that its platforms remain indispensable to brands worldwide. While the metaverse may remain a distant dream, the present belongs firmly to Meta’s advertising empire—an ecosystem of influence and engagement that continues to print money, at least for now.

Meta may not enjoy an outright advertising monopoly—its domain is shared with the likes of Google, Amazon, and even the upstart challengers TikTok and Snapchat—but in the realm of social interaction, its dominance borders on the hegemonic. No other entity has so thoroughly centralized digital communication, threading together the personal and the commercial, the trivial and the profound, into a single, inescapable ecosystem.

As of today, Meta’s platforms—Facebook, Instagram, WhatsApp, Messenger, and Threads—play host to an astonishing 3.35 billion daily users, a figure that accounts for 40% of the planet’s 8.2 billion inhabitants. But this metric understates the company’s true grip on the connected world. Nearly 2.6 billion people, or 32% of the global population, still lack access to the internet. If one considers only those with connectivity—some 5.6 billion souls—Meta’s reach swells to encompass over 57% of the online world.

This is the quiet monopoly: not one of commerce, but of conversation itself. Meta has become the public square, the digital agora where billions gather—not merely to be entertained or sold to, but to exist within a networked society. While competition may flicker at the edges, the architecture of online social life is, for now, unmistakably Meta’s domain.

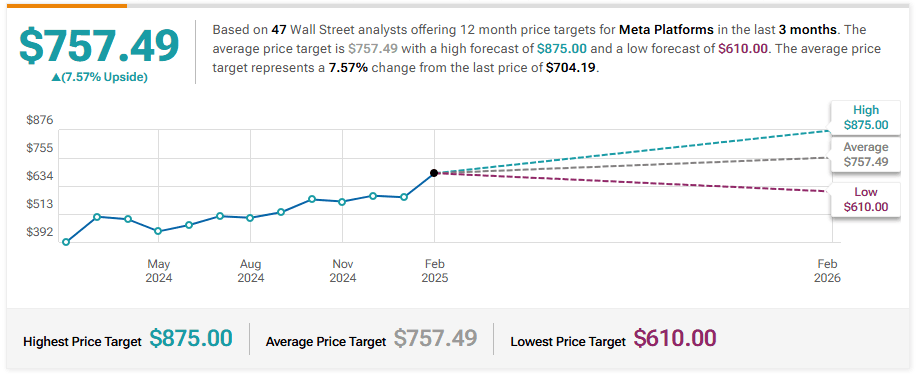

UBS Maintains Buy on Meta Platforms, Raises Price Target to $786

Citigroup Maintains Buy on Meta Platforms, Raises Price Target to $780

Oppenheimer Maintains Outperform on Meta Platforms, Raises Price Target to $800

B of A Securities Maintains Buy on Meta Platforms, Raises Price Target to $765

BMO Capital Maintains Market Perform on Meta Platforms, Raises Price Target to $610

DA Davidson Maintains Buy on Meta Platforms, Raises Price Target to $800

RBC Capital Maintains Outperform on Meta Platforms, Raises Price Target to $800

Goldman Sachs Maintains Buy on Meta Platforms, Raises Price Target to $765

Benchmark Upgrades Meta Platforms to Buy, Maintains Price Target to $820

Cantor Fitzgerald Maintains Overweight on Meta Platforms, Raises Price Target to $790