Online Dating Market Breakdown:

The tide of societal trends has increasingly drawn individuals towards online dating applications, creating a fertile ground for investors to potentially profit from the leading companies in this burgeoning sector.

According to a study by the Pew Research Center, approximately 30 percent of U.S. adults have ventured into the realm of online dating. The numbers are even more striking among young adults, with over half (53 percent) of those aged 18 to 29 having utilized a dating app.

Despite this, the stock prices of major public dating app companies have suffered this year, reflecting a waning interest in online dating among Generation Z. This cohort, it seems, prefers meeting “in real life” (IRL). Furthermore, the dating app market is now saturated, with numerous apps competing for users, leading to a stagnation in the once-rapid user growth, as noted in a Morgan Stanley report earlier this year.

In response, companies have turned towards monetization strategies, particularly through paid subscriptions, which vary in price based on the user’s commitment level. “With strong free offerings, online dating has needed to up its game with compelling features to convert more users to payers,” Morgan Stanley observes. Although revenue continues to grow for these companies, the pace has notably slowed.

Pros:

Growing Market: The online dating industry has expanded significantly, driven by societal acceptance and technological advancements.

Recurring Revenue: Subscription models ensure a steady income stream for companies.

Diverse Demographics: Dating apps cater to a broad range of age groups, preferences, and demographics.

Adaptability: Many platforms have demonstrated an ability to pivot or adapt, introducing new features or expanding their services beyond dating, thus opening additional revenue streams.

Global Reach: Modern dating apps often boast a global user base, allowing for international expansion and growth.

Resilient Market: The dating industry remains relatively resistant to economic downturns, as people continue to seek connections during such times.

Cons:

Changing Consumer Preferences: Trends in the dating world can shift rapidly, and apps that fail to adapt may see diminishing user numbers.

Privacy Concerns: The handling of personal information makes dating apps targets for data breaches, which can severely impact their reputation and stock value.

Regulatory Risks: Regulatory challenges or bans in certain countries or regions can affect market potential.

Dependency on Tech Infrastructure: Issues with app stores, payment gateways, or cloud services can directly impact an app’s availability and revenue.

Monetization Challenges: Balancing effective monetization without alienating users remains a delicate task.

Thus, while the online dating industry presents a compelling growth opportunity, it is not without its substantial risks and challenges. Investors must navigate these complexities to capitalize on the sector’s potential.

Members overview

This is a list of stocks that members asked us to do extra research on none of these are alerts/buy/sell recommendations.

Company: Match Group, Inc

Quote: $MTCH

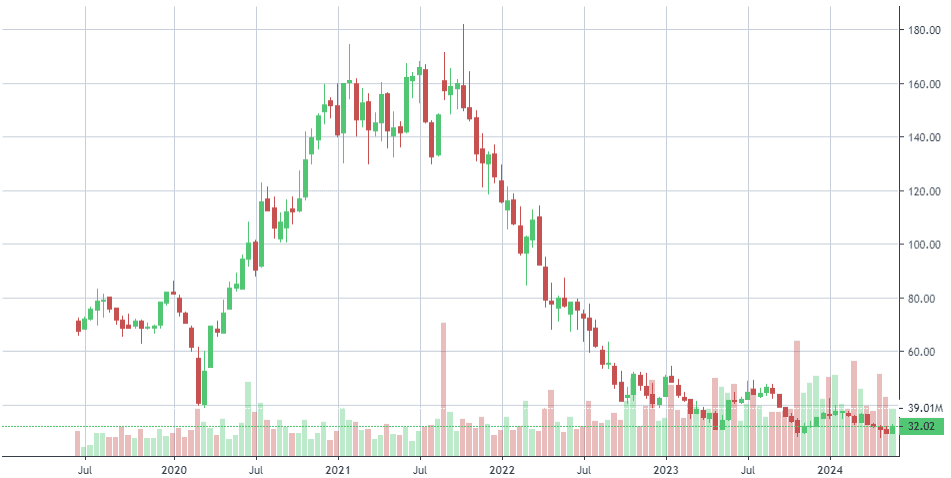

Match Group finds itself in a curious predicament. The stock has suffered notable declines over recent quarters, sparking interest among some investors who see potential value in acquiring shares of this dating app conglomerate at a discount. This sentiment mirrors the current investor approach towards PayPal, where a similar thesis is being applied.

In our view, the situation is multifaceted. On one hand, Match Group has demonstrated a strategic acumen by acquiring valuable assets to maintain its edge over the competition. However, a discernible pattern emerges with each acquisition: the acquired companies enjoy a surge in popularity initially, only to plateau and eventually be overshadowed by newer, trendier market entrants.

Match operates a mature software model, with Tinder as its primary revenue driver. Nevertheless, its high subscription rates do not resonate well with its predominantly male user base, especially under inflationary pressures. Additionally, dating platforms are notoriously plagued by spam accounts, further complicating user engagement and satisfaction.

The narrative takes an intriguing turn with reports of a second activist investor building a significant stake in Match Group’s stock. Anson Funds Management LP, which oversees nearly $2 billion in assets, may attempt to instigate changes within Match’s board of directors. This move could potentially attract retail investors, increasing trading volume. Notably, Elliott Management already commands a substantial $1 billion stake in Match, signaling a burgeoning interest from influential investors.

In conclusion, while Match Group presents an enticing opportunity, the challenges it faces and the evolving landscape of the dating app industry necessitate a cautious and informed approach.

ST: $38-$40

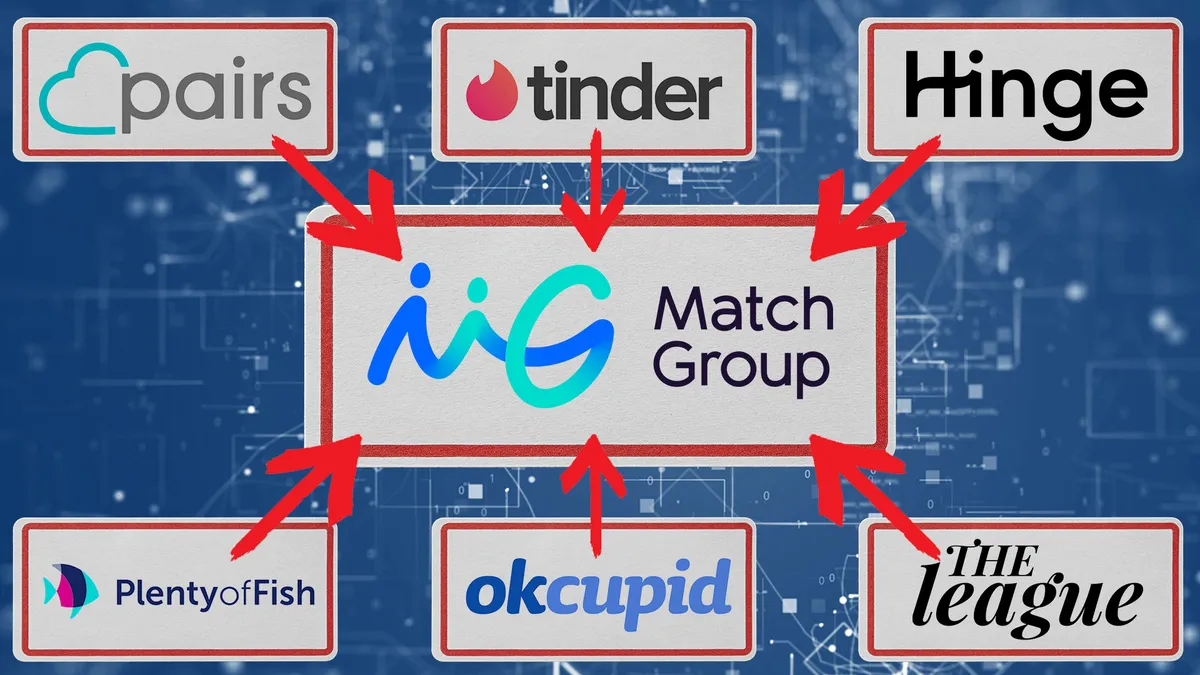

Description: Match Group, Inc. engages in the provision of dating products. Its portfolio of brands includes Tinder, Hinge, Match, Meetic, OkCupid, Pairs, Plenty Of Fish, Azar, BLK, and Hakuna, as well as a various other brands, each built to increase users’ likelihood of connecting with others. Its services are available in over 40 languages to users worldwide. The company was incorporated in 1986 and is based in Dallas, Texas.

Short Interest:

Short Percent of Float 5.60 %

Short % Increase / Decrease -4 %

Match Group stands as the largest and oldest titan in the online dating industry, having strategically expanded far beyond its origins as Match.com through a “roll-up” strategy. Today, it boasts an impressive portfolio of about 45 distinct dating brands, each tailored to various demographics, including age, ethnicity, sexual orientation, and geographic regions.

Founded in the early days of the internet in 1995, Match.com was the cornerstone of what would become a sprawling empire. The business truly flourished with the advent of mobile technology and the development of Tinder, the swipe-based app that revolutionized online dating. Smartphones provided unparalleled access to these platforms, fueling Tinder’s rapid ascent throughout the 2010s and propelling Match Group’s growth. Tinder now lies at the heart of the company’s operations, driving more than half of its revenue and serving as a model for other subscription-based swipe apps. More recently, Match acquired Hinge, an app dedicated to fostering relationships rather than casual hookups.

The decline of Tinder was perhaps inevitable, given the cultural shift in dating app usage. Younger users have increasingly sought serious, long-term relationships rather than the casual encounters for which Tinder is renowned. This shift has propelled Hinge’s popularity among users seeking more meaningful connections.

While Tinder grapples with retaining its paying users, Hinge is poised to become a “billion-dollar revenue business,” marking a significant pivot in Match Group’s strategic landscape.

When Match Group, which reported its earnings, managed to surpass analysts’ estimates provided by LSEG, previously known as Refinitiv. The company posted $881.6 million in revenue, slightly exceeding the expected $880.6 million, and reported earnings of 57 cents per share, three cents above projections.

Despite these encouraging figures, analysts voiced concerns regarding the company’s lower fourth-quarter revenue projections and a decline in the number of paying Tinder users.

Match projected fourth-quarter revenue to fall between $855 million and $865 million, substantially below the anticipated $894 million. This conservative guidance has sparked apprehension among investors, overshadowing the otherwise positive earnings report.

In recent months, Tinder has attempted to bolster its revenue by extracting more from its shrinking base of paying users, evidenced by the launch of a $499 per month plan aimed at elite users. Despite these efforts, Tinder’s revenue forecast for the upcoming quarter suggests stagnant growth, expected to be flat or rise by a mere 1%, ranging from $475 million to $480 million.

Tinder’s paying user base has declined for the sixth consecutive quarter. Conversely, Hinge has seen a rise in members willing to pay for its services. In Q1 2024, Tinder had 10 million paying users, marking a 9% decrease from the previous year. Meanwhile, Hinge’s paying users have surged by 31% year-over-year, reaching 1.4 million.

It is particularly concerning to note a 14% decline in the number of paying users in the U.S. region, a critical market for Match Group. This double-digit drop in payer volume is alarming and underscores broader challenges within the company.

Furthermore, management has yet to make significant strides in deploying redesigns within Tinder’s app, raising questions about the platform’s future growth prospects and strategic direction.

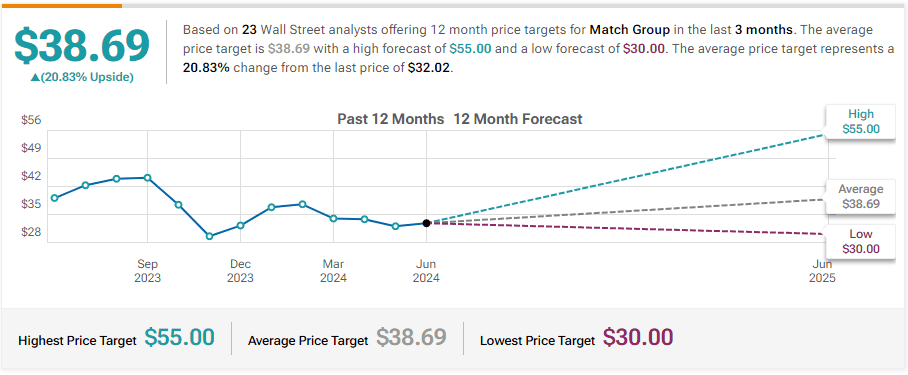

Goldman Sachs Maintains Buy on Match Group, Lowers Price Target to $37

Keybanc Maintains Overweight on Match Group, Lowers Price Target to $44

Deutsche Bank Maintains Buy on Match Group, Lowers Price Target to $38

Wells Fargo Maintains Equal-Weight on Match Group, Lowers Price Target to $30

TD Cowen Maintains Buy on Match Group, Lowers Price Target to $44

RBC Capital Maintains Outperform on Match Group, Lowers Price Target to $33

UBS Maintains Neutral on Match Group, Lowers Price Target to $36

Susquehanna Maintains Positive on Match Group, Lowers Price Target to $45

Company: Bumble Inc

Quote: $BMBL

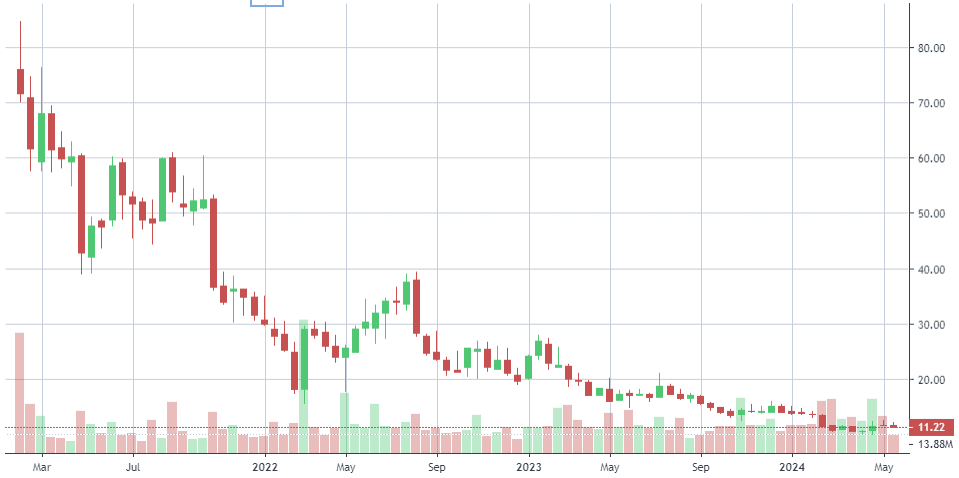

We took a hit on the Bumble IPO, purchasing the stock at $55 and selling in the $30s after several dismal quarters. Despite this, the stock has continued its descent, now trading just above a $1 billion valuation. At its current price, Bumble seems to be trading at fair value. Unlike Match, which boasts several standout apps, Bumble relies primarily on one or two key apps operating in prime time.

While there is potential for BMBL stock to swing higher on earnings beats, we are currently not inclined to re-enter this name. For now, we remain cautious and will watch how the situation unfolds before considering any renewed investment.

ST: $16

Description: Bumble Inc. provides online dating and social networking platforms in North America, Europe, internationally. It owns and operates websites and applications that offers subscription and in-app purchases dating products. The company operates apps, including Bumble, a dating app built with women at the center, where women make the first move

Short Interest:

Short Percent of Float 12.47 %

Short % Increase / Decrease -3 %

Bumble, the brainchild of former Tinder marketing executive Whitney Wolfe Herd, went public in early 2021, capitalizing on the success of Match Group. Like Tinder, Bumble users swipe left or right on potential matches, but with a unique twist: only women can initiate contact. This feature has made the app particularly popular among women and has contributed to a less aggressive user environment compared to other online dating platforms.

Investors initially drove Bumble’s stock price sky-high during its IPO amid the peak of the growth tech stock boom. However, the stock has since fallen below its IPO price, largely due to the broader compression in tech stock valuations rather than any specific shortcomings in Bumble’s performance. The company experienced rapid growth in the first nine months of 2021, with revenue increasing by 34% and adjusted EBITDA margins around 20%, although it remains unprofitable on a GAAP basis.

In February 2022, Bumble acquired Fruitz, a fast-growing European dating app targeting Gen Z, adding to its portfolio which includes Bumble and Badoo, a 2006-founded app that continues to lead in European and Latin American markets. This acquisition suggests that Bumble might be pursuing a roll-up strategy similar to Match Group’s, aiming to expand its reach and diversify its offerings.

Despite revenue climbing from $903.5 million in 2022 to $1.05 billion in the past year, Bumble continues to grapple with significant net losses, recording a deficit of $1.9 million in 2023. The bulk of its revenue is derived from subscriptions and in-app purchases.

Recently, the company announced the layoff of 370 employees, roughly 30% of its workforce, underscoring its struggle to realign operations amid financial challenges. This decision follows the resignation of Bumble’s founder, Whitney Wolfe Herd, from her CEO role last year. She has been succeeded by Lidiane Jones, the former CEO of Slack.

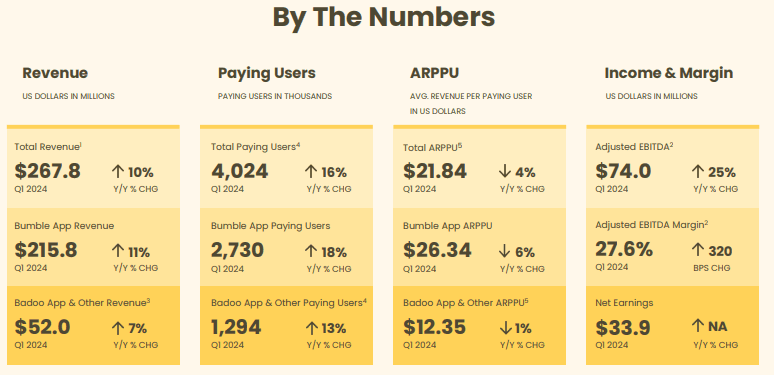

When Bumble released its first-quarter results on last month, It Reported

Revenue of $268 million, marking a 10% year-over-year increase, surpassing management’s guidance.

Adjusted EBITDA of $74 million, a 25% year-over-year increase, exceeding expectations.

A 171.43% surprise on earnings per share (EPS).

A net addition of 42,000 users, slightly above management’s guidance of 30,000 to 40,000.

Despite ongoing sluggishness in top-of-the-funnel trends, management remains hopeful about future growth, especially following the relaunch of the Bumble app. Early post-relaunch results are encouraging, with nearly half of new users engaging with Opening Moves and an uptick in chats and matches.

Investors have shown skepticism, leading to the stock trading at 5x the estimated 2025 adjusted EBITDA. Nevertheless, there is potential for significant upside.

B of A Securities Upgrades Bumble to Buy, Maintains $14 Price Target

Deutsche Bank Maintains Hold on Bumble, Lowers Price Target to $13

Goldman Sachs Maintains Buy on Bumble, Lowers Price Target to $15

Evercore ISI Group Maintains Outperform on Bumble, Raises Price Target to $18

Company: Grindr Inc

Quote: $GRND

Though we have no intention of investing in or buying this stock, it merits attention due to its remarkable user and revenue growth. Additionally, it could become a potential acquisition target, possibly driving the stock to a premium.

Since its initial public offering in 2022, Grindr has encountered financial turbulence. Its stock has plummeted 70 percent since the SPAC debut. After peaking at an IPO high of $71.51, it now languishes at $9.48.

ST: $14

Description: Grindr Inc. operates social network and dating application for the lesbian, gay, bisexual, transgender, and queer (LGBTQ) communities worldwide. Its platform enables LGBTQ people to find and engage with each other, share content and experiences, and express themselves. The company offers ad-supported service and a premium subscription version. Grindr Inc. was founded in 2009 and is headquartered in West Hollywood, California.

Short Interest:

Short Percent of Float 17.75 %

Short % Increase / Decrease 6 %

Grindr disclosed having approximately 13.3 million active monthly users in 2023, as per SEC filings. Their investor relations page further notes an average of 937,000 users subscribing each month.

Following a restructuring phase, Grindr has been surpassing competitors like Match Group and Bumble.

Now, Grindr aims to bolster its revenue by implementing a more aggressive monetization strategy. This includes transitioning previously free features into paid offerings and introducing new in-app purchases, as revealed by company insiders. Additionally, Grindr is developing an AI chatbot capable of engaging in explicit conversations with users, according to reports from Platformer.

Grindr recently announced a collaboration with Ex-human, a startup specializing in customizable chatbots such as AI girlfriends and dating coaches. Initially, Grindr intended to create an AI wingman to assist users in navigating the gay dating landscape.

The company’s profit margins are leading the industry, yet they believe they are currently under-monetizing their user base. Typically, around 15% of monthly active users on a dating app become paying subscribers. Grindr, however, stands at only 7% presently, indicating a potential for doubling revenues, especially considering their scope for further user growth both in the United States and internationally.

Grindr’s third-quarter performance, unveiled in November, showcased a nearly one-fifth increase in average paying users, encompassing à la carte offerings, reaching 962,000. This growth significantly contributed to boosting quarterly revenues by almost two-fifths, totaling $70.3 million.

However, the company faced losses of $11 million during the initial nine months of the year, attributed in part to $8 million incurred in severance costs.

JMP Securities Reiterates Market Outperform on Grindr, Maintains $14 Price Target

Raymond James Initiates Coverage On Grindr with Outperform Rating, Announces Price Target of $14

JMP Securities Initiates Coverage On Grindr with Market Outperform Rating, Announces Price Target of $14

TD Cowen Initiates Coverage On Grindr with Buy Rating, Announces Price Target of $12

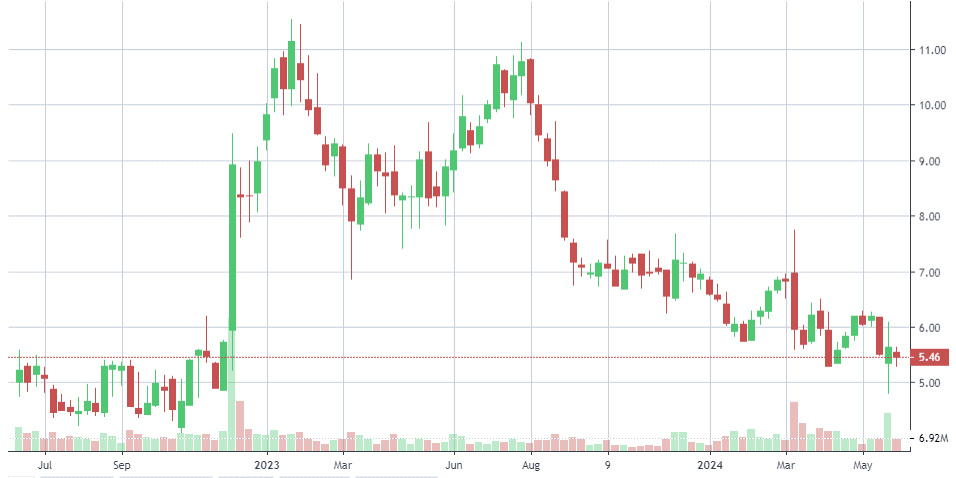

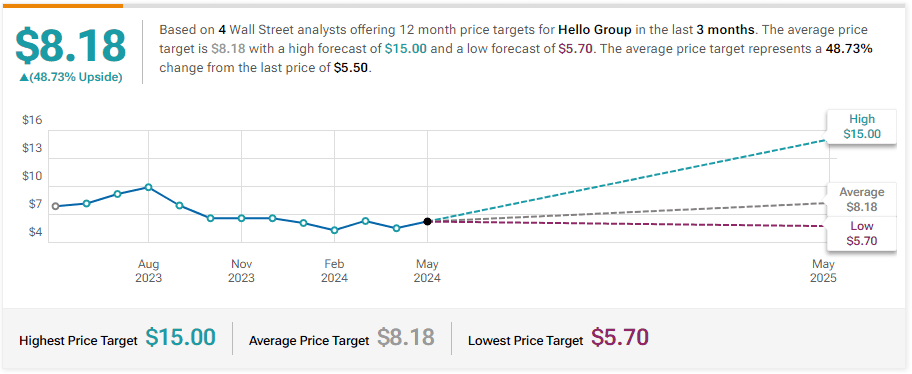

Company: Hello Group Inc

Quote: $MOMO

Momo is a stock that landed on our tape watchlist as we began monitoring Chinese equities a few months back. It’s notoriously challenging to obtain accurate data from China, but MOMO is often likened to the Match Group of China. Nevertheless, we view this solely as a swing trade opportunity with considerable momentum, which is why we’ve included it in this overview.

ST: $8

Description: Hello Group Inc. provides mobile-based social and entertainment services in the People’s Republic of China. It operates in three segments: Momo, Tantan, and QOOL. The company offers Momo, a mobile application that connects people and facilitates social interactions based on location, interests, and various online recreational activities, including live talent shows, short videos, social games, as well as other video- and audio-based interactive experiences, such as online parties, mobile karaoke and user participated reality shows; Tantan, a social and dating application; and other applications under the Hertz, Soulchill, Duidui, and Tietie names.

Short Interest:

Short Percent of Float 2.21 %

Short % Increase / Decrease -9 %

China restricts access to most U.S. social media apps, which is why popular online dating platforms like Tinder and Bumble are unavailable there. This situation has created an opportunity for Hello Group, a company that blends aspects of social media and online dating.

Hello Group’s main offerings include Momo, a social media and video entertainment platform widely used for online dating, and Tantan, a platform similar to Tinder with swipe-based features.

Similar to other Chinese tech firms, Hello Group (formerly Momo) has faced pressure from Chinese authorities, presenting regulatory risks for investors. In 2019, Tantan was removed from multiple app stores, and both Momo and Tantan temporarily halted news feed posts due to concerns about government scrutiny.

These challenges tempered investor optimism for Hello Group, especially after the pandemic slowed business operations, resulting in flat revenue for the first three quarters of 2021. Momo’s user growth has also decelerated, and its live-streaming and video entertainment segments are losing ground to competitors like Bilibili, which continue to experience robust growth.

JP Morgan Downgrades Hello Gr to Neutral, Lowers Price Target to $6

Benchmark Maintains Buy on Hello Gr, Lowers Price Target to $15

Citigroup Maintains Neutral on Hello Gr, Lowers Price Target to $5.7

Benchmark Maintains Buy on Hello Gr, Lowers Price Target to $16