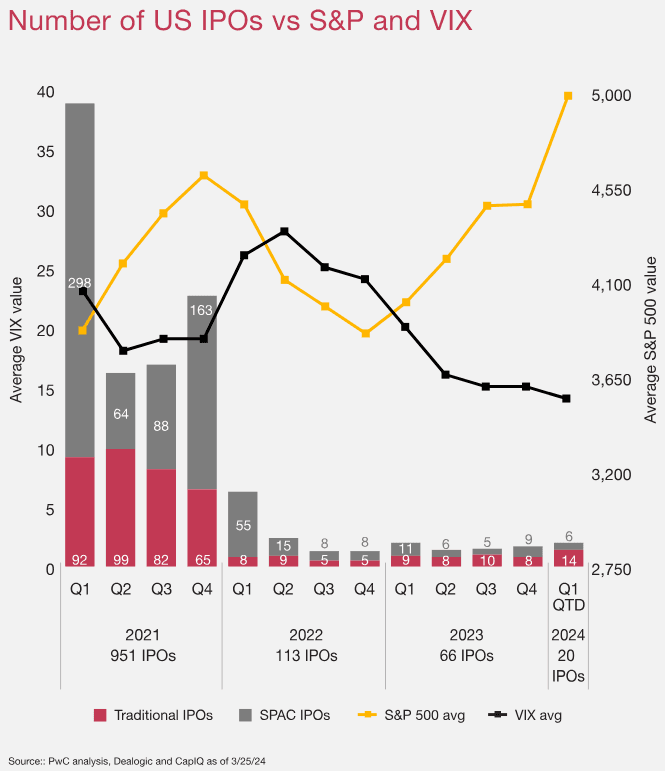

In 2021, Special Purpose Acquisition Companies (SPACs) were ubiquitous. Companies were drawn to SPACs for their ability to expedite the public listing process and often secure higher valuations than traditional Initial Public Offerings (IPOs). A staggering 610 companies utilized SPACs to go public, comprising nearly half of all IPOs that year. The trend even attracted celebrities like Steph Curry, Jay-Z, Serena Williams, and Sammy Hagar.

However, the SPAC frenzy fizzled out in 2022. Only 86 SPACs facilitated company public offerings that year, and by 2023, the number dwindled further to 31 SPACs, representing about 15% of all IPOs.

Then, in January 2024, the Securities and Exchange Commission (SEC) enforced regulations to align SPACs more closely with traditional IPOs. These regulations necessitate increased disclosures regarding sponsor compensation, dilution risk, conflicts of interest, and other critical areas, while imposing greater legal responsibility on target companies.

A Special Purpose Acquisition Company (SPAC) is a firm devoid of operational activities, specifically established to raise capital through an Initial Public Offering (IPO) for the purpose of acquiring or merging with an existing company.

Although SPACs have existed for decades under the moniker “blank check companies,” their popularity surged in recent years. In 2020, 247 SPACs were established with $80 billion invested, followed by a record-breaking 613 SPAC IPOs in 2021. In contrast, only 59 SPACs emerged in 2019.

The momentum behind SPAC IPOs, merger announcements, and completions has slowed in comparison to previous quarters. The first quarter witnessed six SPAC IPOs, 19 SPAC merger announcements, and 20 SPAC merger completions. The SEC’s recent adoption of new rules, aimed at bolstering investor protection by demanding additional disclosure and aligning reporting requisites with traditional IPOs, is expected to continue influencing the frequency of these transactions.

The SPAC IPO market appears to have stabilized, with six SPAC IPOs pricing in the first quarter, over 30% of which came from experienced sponsors re-entering the market. These serial sponsors opted for larger trusts, elevating the average SPAC IPO size for Q1 to $114 million, a 2% rise from Q4 2023 and a substantial 39% increase from the same quarter last year.

Traditional IPOs this quarter have outperformed broader indices by nearly 19%. This could indicate a reopening of the IPO markets, as valuations normalize and a more balanced equilibrium emerges between buyers and sellers, compared to previous periods.

Amid a slowdown in momentum across the broader SPAC/IPO market, numerous firms have reevaluated their prospects for listing. Concurrently, many DE-SPAC companies have faced significant declines. This downturn largely stems from investors withdrawing capital, as the typical enthusiasm for investing in pre-revenue or early-stage companies waned in 2022. Additionally, a notable factor contributing to these declines is the realization that several of these companies may not have been suitable for listing or going public initially.

Nevertheless, despite these challenges, we’ve remained attentive to several potential SPACs and DE-SPAC companies to monitor their trading activities and quarterly earnings reports.

Below is a compilation of companies we believe still hold long-term upside potential, irrespective of whether they were former SPACs and have faced disillusionment from investors.

Company: Blade Air Mobility

Quote: $BLDE

BT: Blade was once a darling among investors during the SPAC frenzy, but like many other stocks, its shares have fallen out of favor. Unlike numerous other SPAC companies, Blade has consistently generated revenue and possesses a viable business model. Two years ago, the company made a pivotal shift, which we’ll delve into shortly, transforming itself and steering towards profitability. Despite its recent struggles, we’ve always viewed Blade as a promising bet on the future of mobility. The daily increase in trading volume indicates a shifting sentiment towards the company. Presently, Blade’s market capitalization stands at a modest $200 million, with a revenue estimate projected to reach $250 million in 2024.

The key point for investors to note is that Blade Air Mobility appears undervalued at its current price, given its market capitalization of only $200 million. The company is strategically positioned to tap into a significant opportunity in air taxi services, particularly with the emergence of new aircraft.

Blade is scheduled to report its earnings next week, and we will be closely monitoring the results for any potential opportunities that may arise based on the outcome.

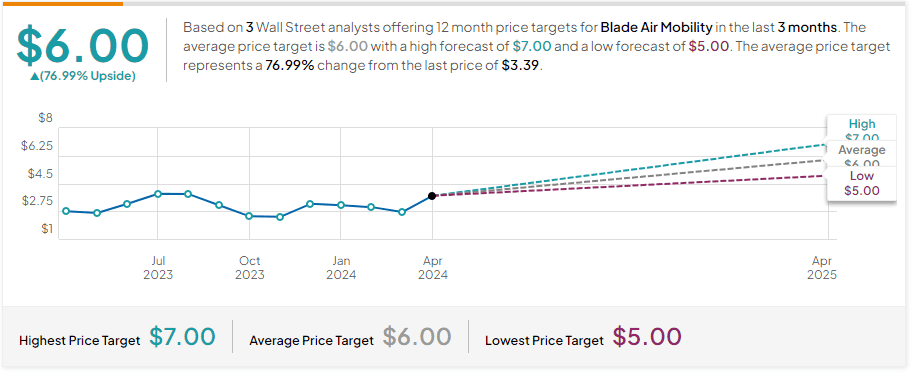

ST: $6-$8 (2024 target)

Description: Blade Air Mobility, Inc. provides air transportation alternatives to the congested ground routes in the United States. It provides its services through charter and by-the-seat flights using helicopters, jets, turboprops, and amphibious seaplanes. The company was founded in 2014 and is headquartered in New York, New York.

Short Interest:

Short Percent of Float 8.01 %

Short % Increase / Decrease 27 %

Like many former SPACs, Blade Air Mobility has significantly expanded its business in recent years, yet its stock continues to trade near all-time lows. Despite the company’s aggressive growth efforts, investors were disappointed with the guidance, although the stock isn’t necessarily trading based on growth expectations.

Blade Air Mobility operates a unique business model, with most costs passed through and experiencing some fluctuations. Although the company reported strong growth in 2023, the market is expressing concerns about revenue and EBITDA profit guidance for the next two years.

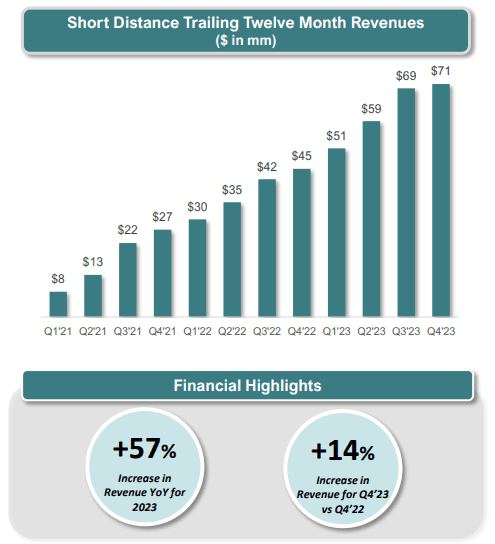

In Q4 ’23, the company saw a 24.5% increase in revenues to $47.5 million. Additionally, the flight margin expanded to 19.0% during the seasonally slow quarter, up from 14.3% in the previous Q4.

Blade’s substantial growth in recent years stems from expanding its existing operations post-acquisitions, especially in the medical market, and reopening businesses after Covid-19 shutdowns. However, the short-distance market’s growth potential is limited due to the current reliance on helicopters and restricted flight operations.

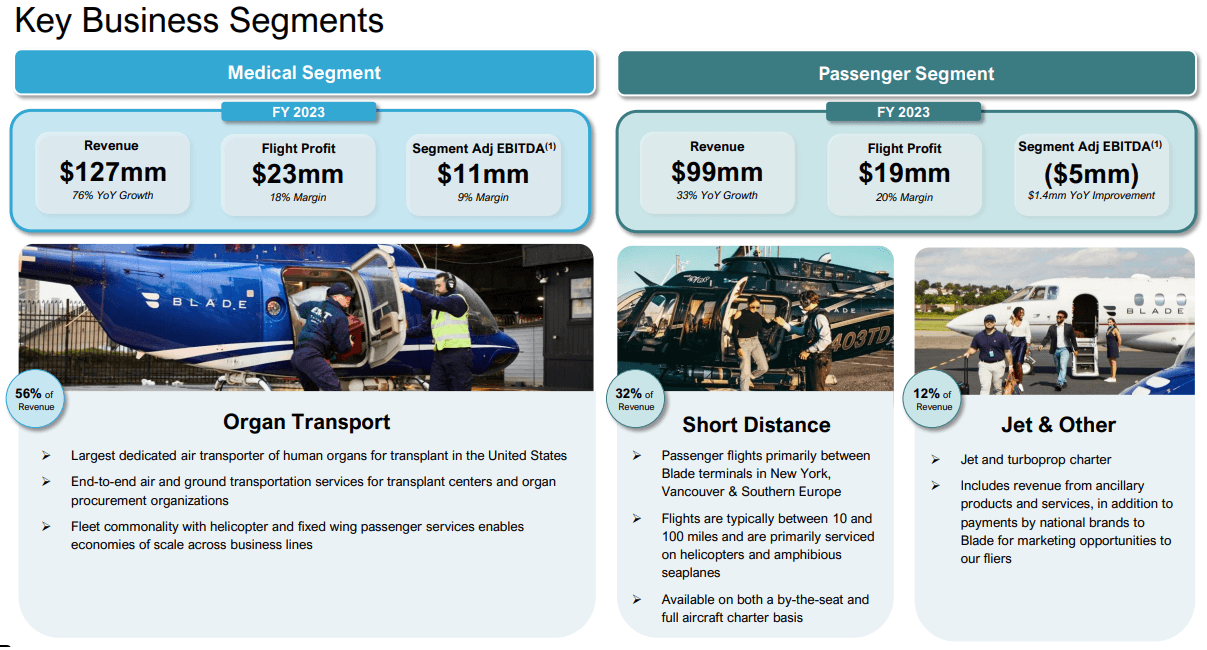

Blade saw a substantial revenue increase in 2023, reaching $225 million, which is over 580% higher than its revenue in 2019.

Interestingly, a significant portion of that revenue, $99 million or 44%, came from transporting vital organs such as hearts, livers, and lungs across the country. This segment has made Blade the largest dedicated air transporter of human organs in the United States. While Blade is known for its premium transportation services, a significant portion of its business revolves around emergency medical transport.

Blade’s core business encounters a seasonality challenge, as highlighted in its 2023 investor presentation. Revenue from passenger flights and flight margins typically peak during the summer months, whereas demand for medical transport remains consistent regardless of weather conditions.

The organ-transplant segment of Blade’s business is experiencing rapid growth compared to other sectors. Revenue from medical transport increased by 48% year-over-year in the fourth quarter of 2023, while short-distance passenger flights saw a 14% increase, and jet/other revenue declined by 32%. This trend indicates the growing importance and profitability of Blade’s medical transportation operations.

Citigroup Maintains Buy on Blade Air Mobility, Lowers Price Target to $8

Credit Suisse Maintains Outperform on Blade Air Mobility, Lowers Price Target to $7

JP Morgan Maintains Overweight on Blade Air Mobility, Lowers Price Target to $5

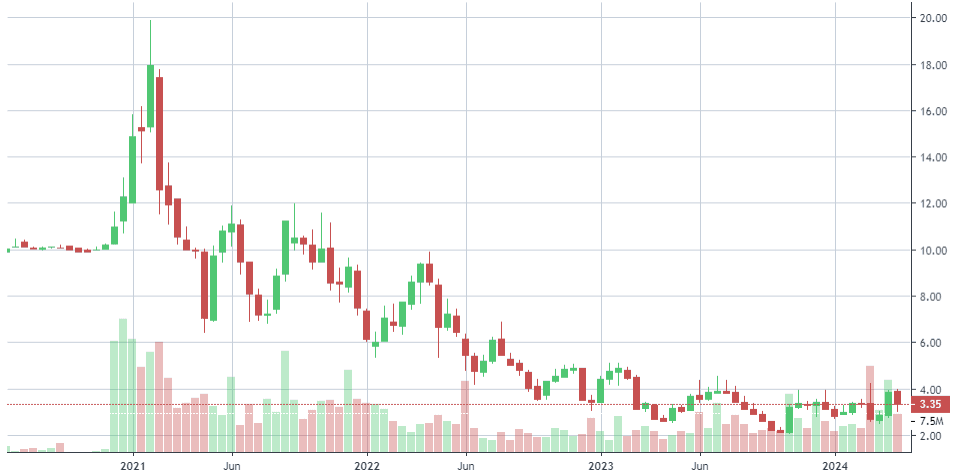

Company: Algoma Steel Group

Quote: $ASTL

BT: Algoma Steel is a recent addition to our radar, as we did not engage with it during the SPAC frenzy of 2020-2021. Nevertheless, we’ve been actively seeking an entry into the industrial sector, and ASTL appears to align well with our criteria.

Algoma Steel is a historic Canadian steel mill with a legacy spanning over a century. Situated advantageously on the St. Mary’s River between Lake Superior and Lake Huron, the company enjoys an independent producer status. Its name, “Algoma,” traces back to the Algonquin Indians and reflects the region where the steel mill is situated in Canadian Sault Ste. Marie.

Having weathered challenges in the 1990s and ultimately filing for bankruptcy in 2001, Algoma underwent significant transformations, including efficiency enhancements and changes in ownership. This year, it re-emerged in the public markets as an autonomous entity. With a production capacity of 2.8 million tons per year from a blend of traditional blast furnace and basic oxygen furnace technologies, Algoma boasts a cost structure that ranks among the most competitive in its industry.

Despite its tumultuous past, we speculate that Algoma’s new leadership and ownership may be positioning the company for potential acquisition. Given the increasing complexities faced by lead operators in Canada and recent developments such as the proposed buyout of the largest steel producer in the USA by a major Japanese steel company, there appears to be a notable shift underway in the industrial landscape. While we’re inclined to monitor Algoma closely, particularly following its upcoming earnings report where a revenue shortfall is anticipated due to a January anomaly, we recognize the potential value it could offer, especially if steel prices escalate.

However, we maintain a cautious stance as we gather more insights into both the sector and Algoma as a company. Despite these reservations, initial indicators suggest promise, even considering its prior listing as a SPAC.

ST: $15

Description:

Algoma Steel Group Inc. produces and sells steel products primarily in North America. The company provides flat/sheet steel products, including temper rolling, cold rolled, hot-rolled pickled and oiled products, floor plate, and cut-to-length products for the automotive industry, hollow structural product manufacturers, and the light manufacturing and transportation industries; and plate steel products that consist of rolled, hot-rolled, and heat-treated for use in the construction or manufacture of railcars, buildings, bridges, off-highway equipment, storage tanks, ships, and military applications. Algoma Steel Group Inc. was founded in 1901 and is headquartered in Sault Ste. Marie, Canada.

Short Interest:

Short Percent of Float %

Short % Increase / Decrease -6 %

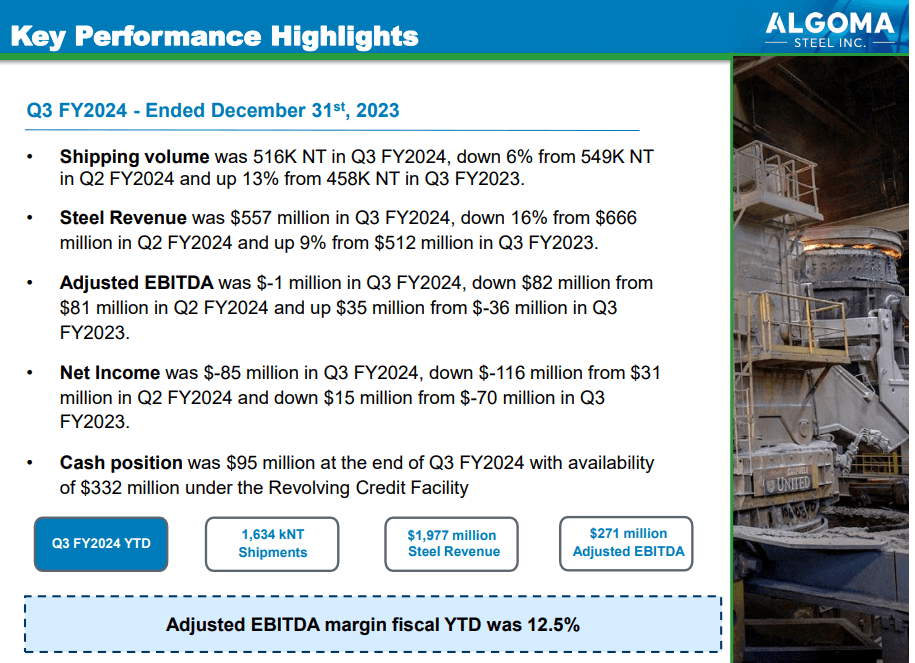

Algoma Steel, currently in the process of transitioning its steel-making approach from Blast Furnace to EAF (Electric Arc Furnace), operates within the cyclical realm of the steel industry, thereby embodying a cyclical business model.

The present iteration of Algoma Steel (ASTL) stems from a 2021 merger with Legato, a special-purpose acquisition company. Consequently, analyzing data predating 2021 may not yield accurate comparative insights.

ASTL functions as the parent entity of Algoma Steel Inc., established in 2016 to assume the assets and liabilities of a Canadian steel enterprise under creditor protection.

In essence, ASTL operates as an integrated steel producer, specializing in sheet and plate products primarily distributed in Canada and the US. As of FYE 2023:

Canada and the US constituted around 40% and 59%, respectively, of its shipment volume.

Hot Rolls and Plates represented approximately 82% and 9% of the shipment volume, with the remaining portion allocated to Cold Rolls.

Given its relatively short operational history, assessing ASTL’s performance solely based on 2022 or 2023 figures may not offer a comprehensive view of its long-term trajectory. This complexity arises from two key factors:

The cyclical nature of the steel market.

The ongoing transformation in ASTL’s steel-making methodology.

Following the business combination, ASTL showcased profitability, registering return on capital figures of 79% and 17% for FYE 2022 and 2023, respectively. However, based on LTM data as of December 2023, the projected return on capital for FYE 2024 stands at approximately 9%.

The diminishing returns, particularly for FYE 2024, are linked to the decline in steel prices. Illustrated in Chart 1, 2023’s steel prices have yet to reach the long-term historical average level.

Looking ahead, returns are anticipated to dip below 9% once prices align with historical averages. However, this projection does not factor in potential cost reductions stemming from the operational shift to EAF technology.

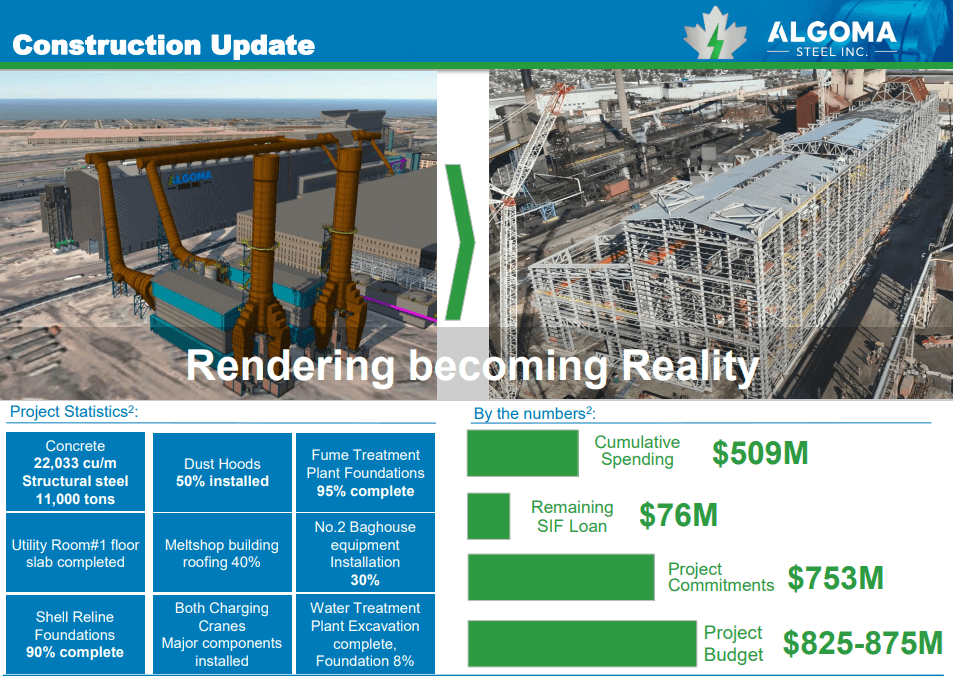

The company is anticipated to gain from robust shipments due to its plate and strip operations returning to standard levels post-upgrades, prioritizing quality enhancements. Furthermore, increased productivity and capacity are set to bolster production. ASTL is also committed to progressing its Electric Arc Furnace initiative, aimed at significantly lowering its yearly carbon emissions.

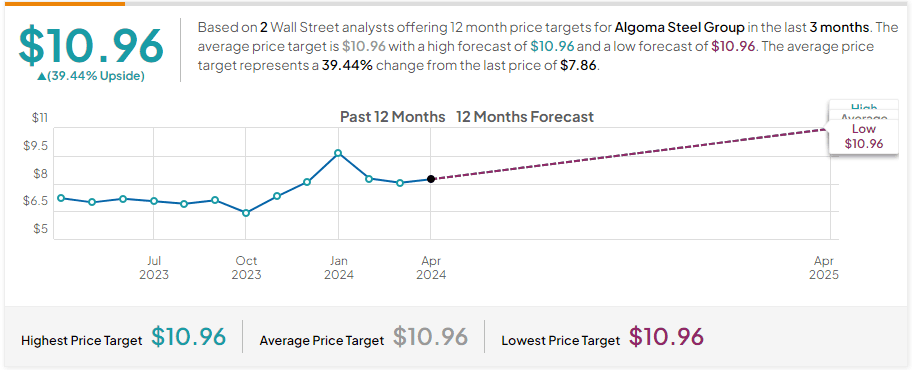

Stifel Maintains Buy on Algoma Steel Gr, Lowers Price Target to $14.25