American Superconductor (AMSC) has experienced a noteworthy 31% surge in its stock price since our recent investment—a commendable uptick that reflects the growing interest in its cutting-edge technologies within the energy sector. Known for its pivotal role in clean energy and power grid modernization, AMSC is helping to define the future of energy with its advanced solutions for renewable integration and smarter grid infrastructure.

At the core of AMSC’s appeal lies its robust technology portfolio, which addresses the pressing challenges of today’s energy systems. Whether enhancing the resilience of aging power grids or advancing the integration of renewable wind energy, AMSC’s offerings are tailored to meet the escalating demands of a cleaner and more efficient energy future. As the global shift towards renewable energy intensifies, AMSC’s technologies are becoming increasingly indispensable—offering solutions that ensure both resilience and efficiency, essential in today’s evolving landscape.

However, AMSC’s ambitions stretch beyond the traditional markets. The company is exploring emerging sectors, signaling its adaptability and readiness to capitalize on opportunities across a broad spectrum of energy technologies. This willingness to expand its horizons positions AMSC as a company with significant upside potential, particularly as government priorities in infrastructure resilience and energy innovation increasingly align with its business model.

In a political environment where policy-driven growth is becoming the norm, AMSC appears well-positioned to benefit from federal initiatives in energy modernization and grid security. Its strategic focus on these high-priority areas could translate into tangible revenue growth and valuable strategic partnerships in the coming years.

AMSC may not boast the headline-grabbing promises of its more flamboyant peers, but it excels quietly in the realm of engineering excellence. By modernizing the energy landscape with understated yet essential technologies, it offers a compelling long-term play for investors with a forward-looking mindset. The company’s steady approach to innovation and growth in a sector defined by transformative change positions it as an attractive option for those with patience and an eye on the broader energy trends.

In a market where many chase fleeting excitement, AMSC’s calm and measured progress may well prove to be its greatest strength. For those of us invested in the future of renewable energy, AMSC presents a dynamic opportunity, albeit one that requires careful consideration of the risks and long-term rewards.

American Superconductor (AMSC) is currently trading at its highest price since early 2021, a period when the stock was swept up in the surge of renewable energy optimism. However, the initial enthusiasm was tempered by investor concerns over the company’s historical losses, despite its potential role in the clean energy infrastructure of the future.

Since mid-2023, AMSC’s stock has mounted a strong recovery. While it briefly found itself caught in the chaotic momentum of the meme stock craze, there are deeper forces at play behind its recent resurgence.

AMSC earns its place as our preferred “MAGA” pick for 2025, a company that not only embodies technological innovation but also positions itself strategically within the context of domestic economic revitalization. While it’s a relatively new name on our radar, AMSC stands poised to leverage significant tailwinds over the coming years, particularly given its critical role in addressing the U.S. energy sector’s future. Today’s double upgrade by analysts, even in the face of broader market uncertainty, reinforces the compelling nature of its narrative.

With the stock now nearing the sell target we outlined last week following our initial purchase, we are adjusting our 2025 price target to $45, with a long-term price objective of $84. The latter may seem distant, but as we know well, in this market, anything is possible.

American Superconductor (AMSC), a U.S.-based company founded in 1987, is dedicated to delivering advanced energy solutions that enhance the reliability, efficiency, and future-readiness of power grids. Specializing in the integration of renewable energy into the grid, AMSC is a pivotal player in modernizing the energy landscape. From improving power flow to designing cutting-edge wind turbine systems, the company is at the forefront of the clean energy movement. Simply put, AMSC’s technologies are essential for ensuring that our power systems run smoothly and sustainably as the world transitions to greener energy sources.

AMSC’s product offerings are neatly divided into three key revenue streams:

Grid Solutions:

The company’s Resilient Electric Grid (REG) technology and D-VAR® systems stabilize power grids while facilitating the integration of renewable energy, ensuring more efficient, resilient grid operations.

Wind Energy Solutions:

AMSC provides advanced electrical control systems for wind turbines, enabling manufacturers to optimize performance and maximize energy output.

Services and Support:

In addition to its core product offerings, AMSC delivers maintenance, upgrades, and system integration services to maintain the long-term efficiency and reliability of energy systems.

The company caters to a wide range of clients, including utilities, renewable energy companies, and industrial sectors, all of whom are increasingly seeking solutions to meet the surging demand for clean energy, while simultaneously ensuring greater energy efficiency and resilience.

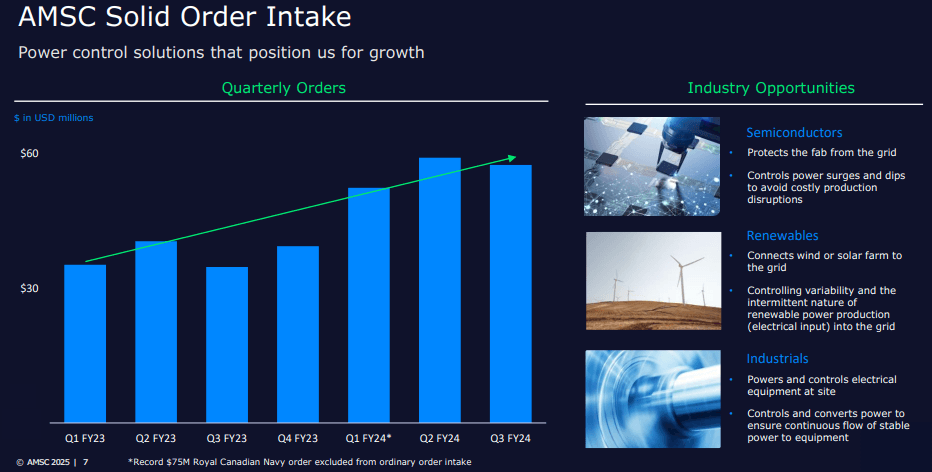

In the third quarter of fiscal year 2024, AMSC reported a record revenue of over $60 million, surpassing its guidance range. This success was fueled by a 55% increase in grid revenue and a 60% growth in wind energy revenue compared to the previous year. The company has secured over $57 million in new orders, spanning markets such as renewables, industrials, utilities, and even the military.

On the financial front, AMSC ended the quarter with $80 million in cash, underscoring its strong financial health. The company has now posted two consecutive quarters of net income and six consecutive quarters of positive operating cash flow, a promising sign for long-term viability in a rapidly evolving sector.

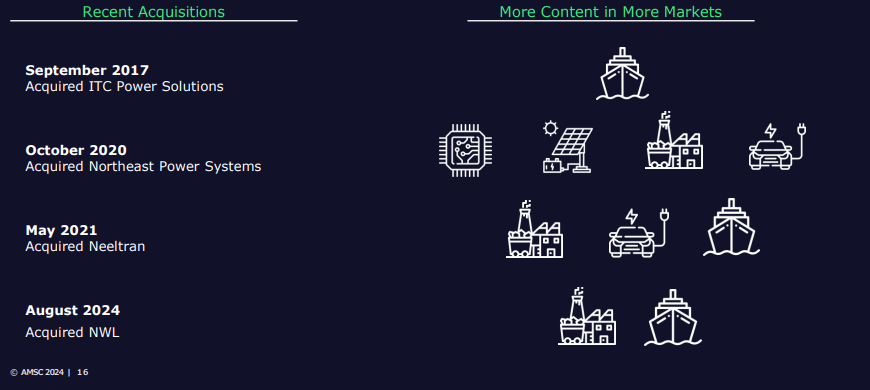

While AMSC has not aggressively pursued acquisitions, the company has substantially bolstered its portfolio through strategic collaborations and partnerships. These alliances have allowed AMSC to integrate cutting-edge technologies, particularly in grid stabilization and wind energy, working alongside regional power companies and wind turbine manufacturers to enhance its solutions.

Under the stewardship of CEO Daniel P. McGahn, AMSC has cemented its position as a prominent force in the clean energy and grid modernization sectors. The company’s overarching vision revolves around creating technologies that not only increase the reliability and efficiency of power grids but also advance the global transition to renewable energy. By emphasizing innovation, avoiding acquisitions in favor of partnerships, and strategically expanding into emerging markets, AMSC remains committed to leading the charge in the global energy transition.

In June 2024, the company made a significant move by securing a $75 million contract with the Canadian Navy to expand its Ship Protection Systems (SPS). This marked AMSC’s first delivery of such systems to an allied navy, further solidifying its foothold in both military and energy sectors.

From a financial standpoint, AMSC has focused on diversifying its revenue streams, balancing product sales with long-term service agreements. In fiscal year 2023, the company posted non-GAAP net income and positive operating cash flow, propelled by robust revenue from sectors including renewables, military, and semiconductors. Notably, approximately one-third of AMSC’s sales were derived from renewable projects, 15% from metals and mining, and 10% from the semiconductor industry.

This financial stability, coupled with its commitment to reinvesting in R&D, positions AMSC well to continue thriving in an energy landscape that is rapidly evolving. The company’s ongoing reinvestment into research and development will ensure it remains at the forefront of technological advancement as the energy markets continue to transform.

For Q3 2024, American Superconductor (AMSC) reported total revenue of $61.4 million, a significant increase from the $39.4 million posted in the same quarter of the previous year.

Grid revenue, which accounts for a dominant 85% of total sales, surged 56% year-over-year, reflecting robust demand for its resilient grid technologies. Meanwhile, wind revenue, making up the remaining 15% of total revenue, saw an even sharper growth of 58% year-over-year, underscoring the increasing reliance on renewable energy solutions.

The company’s gross margin improved to 27% in Q3 2024, up from 25% in the prior year, signaling better operational efficiency despite rising input costs. However, operating expenses, which encompass R&D and SG&A, rose to $14.6 million, up from $10 million in the year-ago period, reflecting AMSC’s continued investment in expanding its technology portfolio.

On the profitability front, non-GAAP net income reached $6 million ($0.16 per share), compared to a modest $900,000 ($0.03 per share) in the same quarter last year. Net income also flipped from a loss of $1.6 million ($-0.06 per share) in Q3 2023 to a positive $2.5 million ($0.07 per share) in Q3 2024.

AMSC’s cash position stood at $80 million at the close of Q3 2024, up slightly from $74.8 million at the end of Q2 2024, indicating stable liquidity. The company generated $5.9 million in operating cash flow during the quarter, while CapEx was contained at $500,000.

In terms of new business, AMSC secured over $57 million in new orders during the quarter, with 75% coming from its grid business and the remaining 25% from its wind solutions. This has contributed to a 12-month backlog of over $200 million, and a total backlog exceeding $300 million, signaling solid demand for the company’s advanced energy solutions.

For the fiscal year, American Superconductor (AMSC) reported revenue of $146 million, up 35% year-over-year, driven by robust growth in both its wind and grid sectors. Wind revenue more than doubled, growing over 100%, while grid revenue saw a nearly 30% increase, reflecting heightened demand for the company’s advanced energy solutions.

On the profitability front, AMSC posted a non-GAAP net income, signaling significant progress in becoming a more profitable entity. While specific net profit margins were small, the overall performance across its core sectors suggests positive profitability, underpinned by strong execution and growth.

Operating expenses rose as AMSC continued to invest in R&D and expanded its personnel base to support its strategic focus on grid stabilization and renewable energy solutions. These investments are expected to lay the foundation for long-term growth.

The company also posted a positive EBITA, reflecting solid core earnings, driven by new orders and improved financial management. This positions AMSC well for future expansion, particularly in the face of rising demand for modernized energy infrastructure.

At the close of the year, AMSC boasted total assets of over $90 million in cash, a notable achievement that underscores its solid financial footing. This strong liquidity provides the company with the capital necessary to support large-scale projects in the grid and wind energy spaces.

Equally important, the company’s total liabilities saw improvement, with AMSC actively managing and reducing debt to strengthen its balance sheet. This focus on long-term sustainability enhances investor confidence.

As for cash and short-term investments, AMSC reported a $72 million cash position, up substantially from the previous year, providing it with ample liquidity for future growth initiatives.

Finally, the company reported positive free cash flow, marking a substantial turnaround from prior years, further bolstering its ability to fund ongoing and future projects as it continues to capitalize on the energy sector’s transition toward cleaner, more efficient solutions.

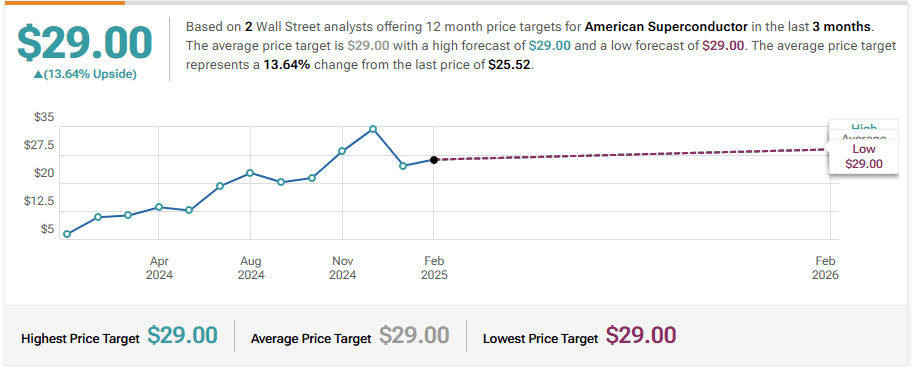

Oppenheimer Maintains Outperform on American Superconductor, Raises Price Target to $39

Roth MKM Reiterates Buy on American Superconductor, Maintains $29 Price Target

Craig-Hallum Reiterates Buy on American Superconductor, Maintains $33 Price Target